Introduction

Richard D. “Rich” Kinder is a defining figure in North American energy infrastructure and in Houston’s civic life. Over a multi-decade career, he moved from practicing law to operating at the highest levels of energy companies and then to building a public company that owns and operates one of the continent’s largest pipeline and terminal networks. Kinder’s career looks, in many ways, like an engineered data pipeline: a small high-quality seed asset was ingested, standardized, scaled, and repeatedly augmented until the resulting platform delivered large, relatively predictable cash flows to investors.

Kinder’s public profile blends corporate achievement with civic patronage. Alongside the business narrative, Rich and Nancy Kinder have used the Kinder Foundation to fund large, visible projects, such as parks, greenways, education initiatives, and, most recently (2026), a $150 million lead gift to establish the Kinder Children’s Cancer Center, a partnership between Texas Children’s Hospital and UT MD Anderson Cancer Center. This profile walks the reader through Kinder’s biography, the architecture of Kinder Morgan’s growth, how his personal wealth is derived and reported, the foundation’s civic footprint, major criticisms and governance questions, and practical lessons for founders and investors. Where the narrative interfaces with facts that can and should be verified, readers are pointed to company filings, primary press releases, and major reportage.

Quick facts

- Full name: Richard D. Kinder.

- Date of birth: October 19, 1944. Age (2026): 81.

- Birthplace: Cape Girardeau, Missouri, U.S.

- Known for: Co-founder & Executive Chairman, Kinder Morgan.

- Estimated net worth (2026): Low-to-mid $10 billion range (different trackers use different methodologies and market valuations).

- Major philanthropic vehicle: Kinder Foundation (parks, education, health). 2026 lead pledge: $150M for the Kinder Children’s Cancer Center.

Early life and education: tokenization of a formative context

Born and raised in southeast Missouri, Richard Kinder grew up in a working-class household and followed a traditional Midwestern educational path into law. He attended the University of Missouri, earning both an undergraduate degree and a Juris Doctor (JD). That legal foundation is central to the rest of the career vector: law school offered Kinder the capacity for contract literacy, regulatory reading, and structured thinking abilities that proved essential when negotiating pipeline contracts, structuring corporate entities, and navigating complex M&A and tax treatments.

From an NLP metaphor: the JD gave Kinder a robust tokenizer, a way to break down complex legal and commercial language into discrete elements, and this allowed him to read and synthesize the “language” of energy contracts and regulation with unusual fine-grained.

Career journey step by step

Enron years and executive rise (pre-1996)

Kinder’s professional climb moved him from practice into executive Ranks within the gas pipeline and energy sector, culminating in senior leadership roles at Enron, where he served as President and Chief Operating Officer. Those years exposed him to large-scale dealcraft, creative financing structures, and high-velocity M&A activity. While Enron later collapsed after accounting scandals that became a corporate governance touchstone, Kinder’s departure in 1996 separated his subsequent trajectory from the firm’s later legal and financial unraveling, though the association occasionally resurfaces in reputational discussions.

Why it matters: Operating inside the fast-paced environment of Enron gave Kinder first-hand experience of structuring big deals, negotiating long-term contracts, and building networks, all of which were inputs into his later platform strategy.

The breakaway and the birth of Kinder Morgan (1997)

In 1997 Rich Kinder and partner William V. Morgan purchased Enron’s liquids pipeline business with a relatively modest cash outlay for an asset with deep operational leverage. That purchase was the seed that became Kinder Morgan. From there, Kinder used both acquisitions and creative corporate and tax architectures to roll up pipeline and terminal assets across North America.

In ML parlance: Kinder took a high-signal seed input and applied repeated parameter updates (acquisitions, standardization, yield optimization) until the model converged on a large, predictable cash-flow generator.

MLP engineering and the growth playbook

A central financial tool in the company’s expansion was the Master Limited Partnership (MLP) , an energy-sector favorite because of tax and yield advantages for investors. (Note: MLP in energy = Master Limited Partnership; in machine learning MLP = multi-layer perceptron two acronyms, same letters, different layers.) Kinder used MLPs and related structures to attract yield-seeking capital and to lower the company’s cost of capital, while continuing to expand asset scale through targeted acquisitions.

The core commercial thesis was simple and robust: buy fee-based midstream assets (pipelines, terminals, storage) that deliver long-duration contracted cash flows, standardize operations and maintenance across assets to reduce unit costs, and return cash to owners.

How Kinder Morgan grew assets, scale, and the platform architecture

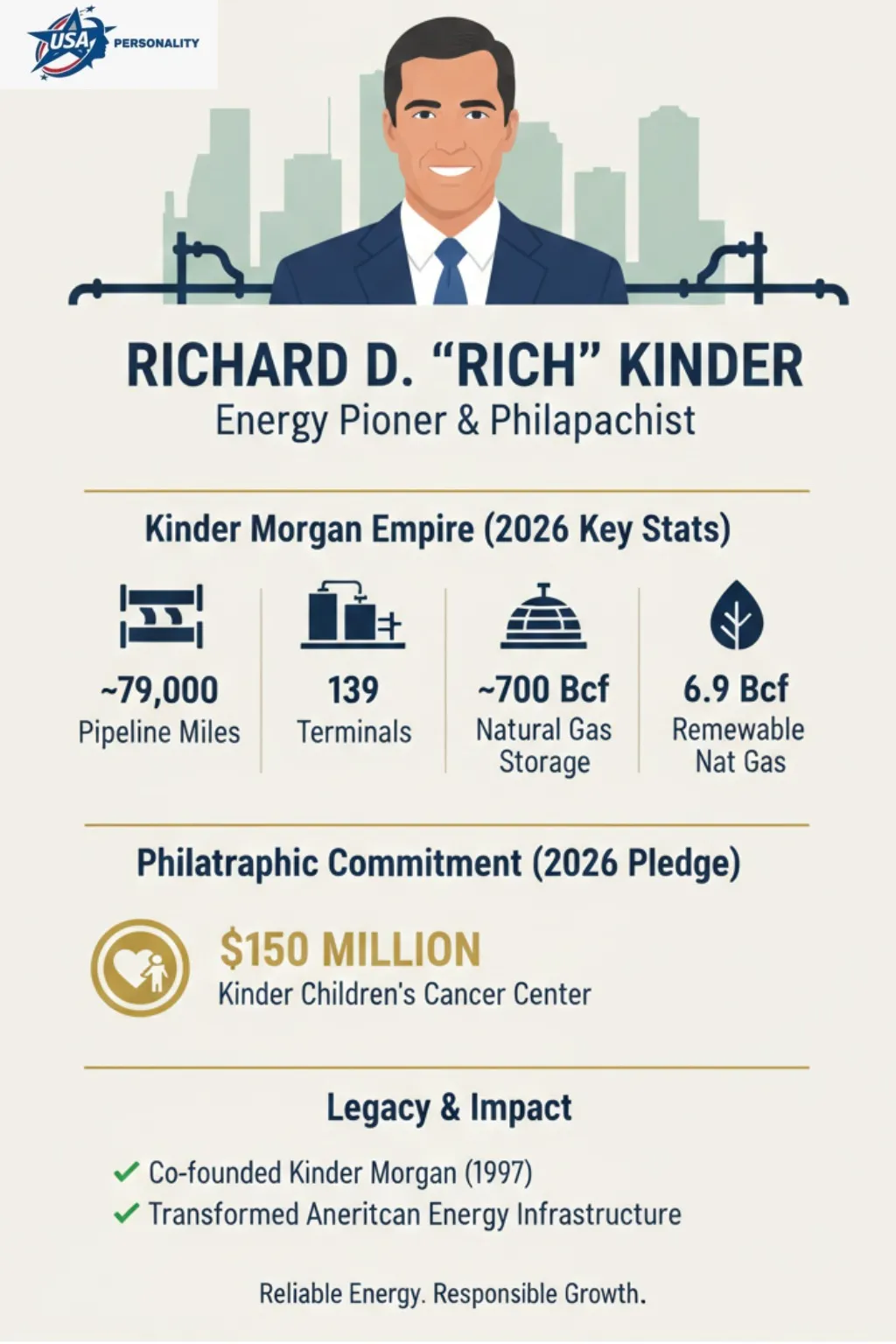

Kinder Morgan’s 2026 profile is that of a network utility: fixed assets with high initial capex and long operational lives, where incremental throughput scales revenue without equal incremental capital. As of 2026, the company reports a large footprint:

- ~79,000 miles of pipelines.

- 139 terminals.

- ~700 Bcf of working natural gas storage capacity.

- Renewable natural gas generation capacity (gross production) of roughly 6.9 Bcf per year.

From a platform perspective, those numbers exemplify network effects: once permitting and right-of-way are in place, marginal throughput additions are less costly than building equivalent greenfield infrastructure. Kinder Morgan’s strategy was to acquire existing infrastructure and operate it under a centralized operating model that generated economies of scale in maintenance, capital allocation, and regulatory compliance.

Net worth, ownership, and compensation decoding the equity vector

Richard Kinder’s wealth is primarily equity-based. Unlike CEOs whose compensation is dominated by large cash salaries, founder-executives like Kinder typically derive value from large ownership stakes and from company cash distributions that flow to owners. Wealth tracking services (Forbes, Bloomberg) apply different models and timing to estimate net worth, which explains day-to-day divergence in headline numbers. In 202,5 such trackers place Kinder in the low-to-mid $10 billion range; those estimates should be read as model outputs sensitive to market price inputs.

For exact figures on ownership percentages, board pay, and proxy disclosure, the company’s SEC filings and investor presentations are the authoritative primary sources.

The Kinder Foundation’s civic embedding and major gifts

The Kinder Foundation is Richard and Nancy Kinder’s principal Philanthropic vehicle. Its strategy is place-based, focused on a handful of large, transformative investments rather than many small grants. Major areas of interest include urban green space (parks and riverfronts), education, and health care. Historical gifts from the foundation include Discovery Green, Memorial Park improvements, Buffalo Bayou revitalization projects, and the Kinder Land Bridge.

This pattern of large, concentrated gifts is intentionally strategic: a single, sizable capital project can catalyze broader civic change in a way that many small grants do not. For the Kinder family, philanthropy has functioned as an extension of legacy building shaping Houston’s physical and institutional landscape.

The $150M Kinder Children’s Cancer Center (2026) data point & implications

On May 14, 2025, the Kinder Foundation announced a $150 million lead gift to launch the Kinder Children’s Cancer Center, a joint pediatric oncology initiative between Texas Children’s Hospital and UT MD Anderson Cancer Center. The donation was framed as seed capital for construction, research, and program expansion and was widely covered in institutional press releases and local reportage.

Why this matters: the gift aligns with the foundation’s preference for large-scale investments in health and civic institutions. For Houston, the pledge is a headline civic asset both symbolically and practically significant for pediatric cancer research and care.

Major works & achievements distilled outputs

- Platform scale: Scaling Kinder Morgan into one of North America’s largest midstream companies, with vast pipeline miles and a substantial terminal network.

- Playbook execution: Repeated acquisitions, use of MLP structures, and a disciplined focus on fee-based assets produced a stable cash generation model attractive to yield investors.

- Civic philanthropy: Large, visible gifts that materially reshaped parts of Houston’s public realm and healthcare infrastructure, culminating in the 2026 $150M pediatric cancer pledge.

Personal life, low public profile, high civic visibility

Richard Kinder is married to Nancy Kinder (married 1997). The Kinders reside in Houston and are notable for their philanthropic footprint there. Kinder keeps a relatively low personal media profile; most public information about the family and their gifts appears through the Kinder Foundation and institutional press statements. Kinder also has adult children from an earlier marriage and has engaged in Political Contributions, which are public records and periodically enter the broader narrative around civic influence.

Leadership style strengths mapped to outcomes

Strengths

- Deal orientation: Kinder is widely regarded as a skillful dealmaker, able to identify assets that fit the company’s operational template.

- Cash focus: The business model prioritized fee-based assets with predictable contractual flows, which supported stable distributions to investors.

- Long-term, disciplined scaling: Kinder combined financial engineering and disciplined acquisitions to scale while preserving a stable income profile for shareholders.

Analogy (NLP): Kinder’s leadership resembles an inference engine that prioritizes low-variance predictions; he designs a portfolio of assets with low forecast error for cash flow, then optimizes their integration to reduce operational noise.

Criticisms & controversies counterfactuals and risk signals

Founder-led governance risks: Concentrated founder influence can challenge independent board oversight and raise questions about compensation, succession planning, and accountability. Critics argue that concentrated control requires stronger external checks.

Environmental and regulatory scrutiny: Fossil-fuel infrastructure inherently draws environmental scrutiny: pipeline leaks, emissions, terminal operations, and land-use conflicts have led to regulatory actions and fines at different times across the industry. These are systemic risks for midstream operators.

Enron association: While Kinder left Enron before the company’s collapse, critics sometimes raise his Enron-era tenure in reputational discussions. Balanced reporting should note Kinder’s exit timeline and focus on documented regulatory records.

Comparison table: Kinder Morgan vs. a typical midstream peer (conceptual)

| Feature | Kinder Morgan (KMI) (2026) | Typical midstream peer |

| Pipeline miles | ~79,000 miles | Usually 10k–40k miles |

| Terminals | 139 terminals | Often 20–120 terminals |

| Business Model | Pipelines, terminals, storage, some renewable natural gas | Pipelines + storage + gathering (varies) |

| Corporate history | MLP-heavy evolution → consolidated corporate structure | Varies; some remain as MLPs |

| Public controversies | Regulatory fines, environmental scrutiny | Varies |

Pros & Cons

Pros

- Exceptional capacity for deal execution and scale.

- Large civic donations that materially shaped Houston’s public life.

- Stable business model for income-oriented investors.

Cons

- Concentrated control and governance questions that accompany founder influence.

- Environmental and community impacts that are inherent to fossil-fuel infrastructure.

- Reputation issues linked by some commentators to Enron tenure (contextual nuance matters).

Timeline selected life events

- 1944: Born October 19, Cape Girardeau, Missouri.

- 1966–1968: University of Missouri, BA and JD.

- 1980s–1996: Career across gas transmission firms culminating in senior roles at Enron.

- 1996: Leaves Enron.

- 1997: Kinder Morgan was founded after the purchase of Enron’s liquids assets.

- 2014–2015: Kinder listed on billionaire lists; steps down as CEO in 2015 but remains chairman.

- 2026: Kinder Foundation pledges $150M to launch the Kinder Children’s Cancer Center.

A step-by-step look at how Kinder built the empire

- Learn the domain. Kinder’s legal and operational background provided high-quality domain knowledge.

- Acquire a seed asset. The 1997 purchase of Enron’s liquids pipelines provided a scalable starting point.

- Choose the right financial controls. Use of MLPs and related structures lowered capital costs and attracted specific investor types.

- Roll up fragmented assets. Buy many midsized pipes and terminals, standardize operations, and integrate under a common platform.

- Prioritize predictable cash flow. Focus on fee-based (contracted) revenue streams rather than merchant exposure.

- Translate wealth into civic legacy. Use a concentrated philanthropic strategy to create lasting public assets.

Examples & case studies

Example: The roll-up play

Imagine buying a 100-mile liquids pipeline that generates predictable fees under long-term contracts. Rather than build new pipes (capex-intensive and slow), acquire additional similar lines, centralize back-office operations, and realize per-mile cost savings. Repeat this across many acquisitions to realize scale advantages.

Example Philanthropic Impact

The Kinder Foundation’s approach to parks and medical centers favors transformational projects over many small grants. Their large gifts to Discovery Green and the $150M pediatric cancer pledge show a preference for concentrated investments that can change a city’s experiential and institutional fabric.

FAQs

A: Richard D. Kinder is the co-founder and executive chairman of Kinder Morgan, Inc., and co-founder of the Kinder Foundation.

A: In the late 1990s, Rich Kinder and William V. Morgan bought Enron’s liquids pipeline assets and used them to roll up pipelines and terminals into Kinder Morgan, using MLPs and acquisitions to grow.

A: Estimates vary with market prices. Major trackers like Forbes and Bloomberg list Kinder’s net worth in the low-to-mid $10 billion range in 2026. For live updates, check the Bloomberg Billionaires Index or Forbes 400.

A: The Kinder Foundation focuses on parks, green spaces, education, and health-care projects in Greater Houston and, in 2026, made a $150M lead gift to start the Kinder Children’s Cancer Center.

Conclusion

Richard Kinder’s arc from a lawyer with granular contract literacy to the architect of a continent-spanning midstream platform is a case study in aligning deep domain knowledge with a repeatable acquisition and integration Playbook. Kinder Morgan’s architecture emphasized fee-based, long-duration assets that, when networked together, delivered predictable cash flows attractive to income investors. Wealth generation for Kinder flowed from equity ownership and distribution-oriented returns rather than an outsized cash salary.

Philanthropically, the Kinder Foundation demonstrates how a donor can translate corporate wealth into a visible civic legacy. The 2026 $150M pledge for the Kinder Children’s Cancer Center is consistent with that pattern. Simultaneously, Kinder’s model is not without tradeoffs: concentrated founder control invites governance scrutiny, and the environmental footprint of fossil-fuel infrastructure brings ongoing regulatory and social risk.

For entrepreneurs and investors seeking to learn from Kinder’s playbook: combine domain expertise, start with high-quality seed assets, choose financial structures that align with your capital base, scale through disciplined acquisitions, and be explicit about the tradeoffs, governance, environmental externalities, and public perception that will accompany growth.