Introduction

In the global LNG boom, where billion-dollar projects hinge on timing, contracts, and execution, Robert “Bob” Pender stands out as a founder who didn’t come from engineering—but from the legal architecture that makes energy deals possible. As co-founder of Venture Global, Pender helped turn a project-finance mindset into a scalable LNG business model built on modular construction, long-term contracts, and speed to market.

What makes his story especially relevant in 2026 is not just the company’s rapid rise, but the scrutiny that followed. After Venture Global’s 2025 IPO, increased transparency around insider trades, arbitration disputes, and regulatory timing pushed Pender into a sharper public spotlight. This article breaks down his career, the strategy behind Venture Global’s growth, and the governance questions investors are now paying close attention to—separating facts from headlines and giving you a clear, practical understanding of his impact.

Quick facts

- Full name: Robert (Bob) Pender

- Known as: Bob Pender

- Date of birth / Age / Birthplace: Not publicly disclosed (public profiles emphasize professional record)

- Nationality: American (inferred from filings and career)

- Profession: Energy lawyer, entrepreneur, Executive Co-Chairman & Co-Founder, Venture Global Inc.

- Notable: Co-founded Venture Global (2013); architect of modular LNG build strategy; involved in the Jan 2026 IPO and subsequent press/regulatory scrutiny.

- Public persona: Private on personal life; public coverage centers on project execution, offtake contracts and governance questions.

Childhood & early life

Public sources contain limited human-interest data about Pender’s childhood or schooling. Most profiles begin with his work as a project-finance attorney. From a data completeness perspective, the missingness is explicit: birthdate and hometown fields are blank in public profiles. This article, therefore, focuses on professional milestones that are verifiable in corporate disclosures and public reporting.

Key professional signals from early career:

- Training and practice in project finance at major law firms.

- Experience in structuring cross-border energy and infrastructure deals.

- Skills that map directly to LNG project needs: long-term contract drafting, lender protections, risk allocation.

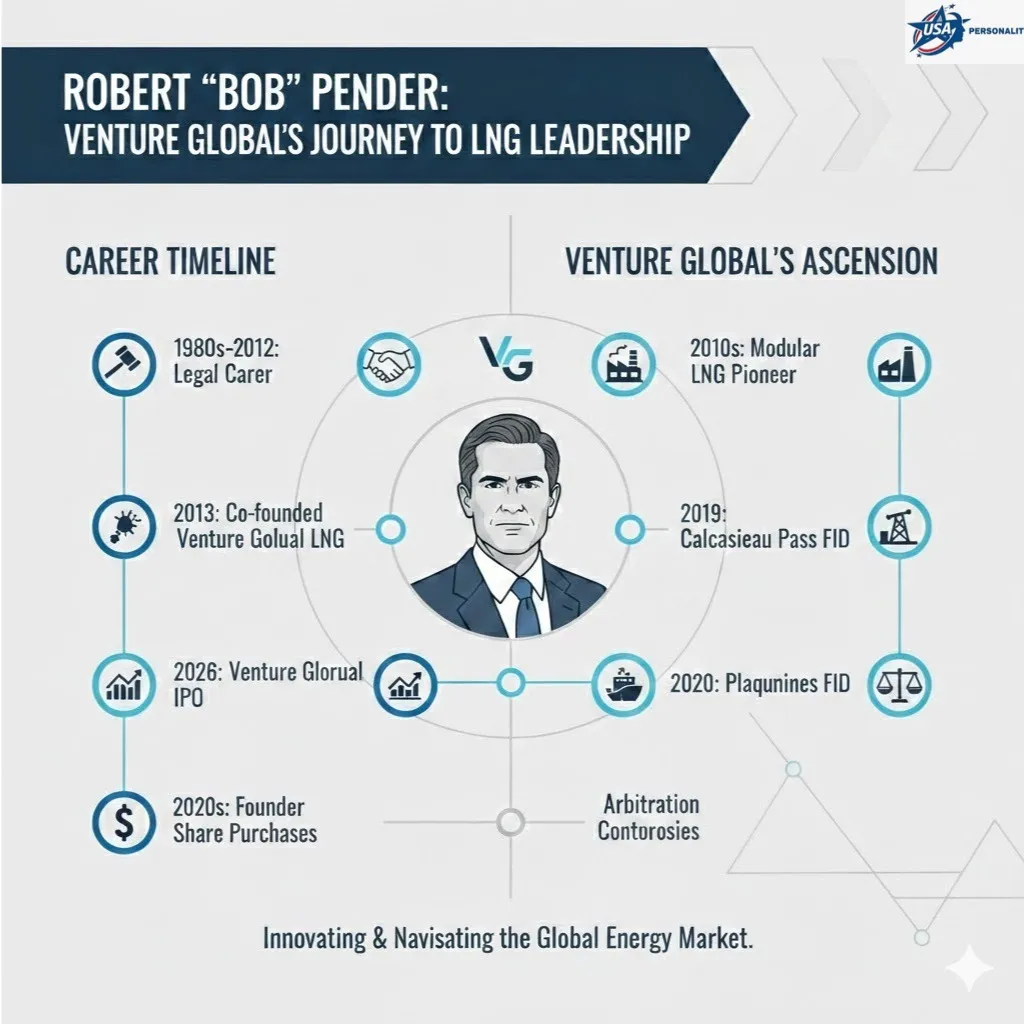

Career journey from Big Law to energy entrepreneur

Pender’s path reflects strong feature engineering: he took institutional skills (contract architecture, lender negotiation, structured finance) and transformed them into operational playbooks for capital-intensive projects. In NLP terms, he converted high-value tokens (legal expertise) into transferable embeddings for energy project development.

Typical competencies

- Modeling long-term cash flows and lender protections.

- Negotiating multiparty agreements across sponsors, lenders, contractors, and offtakers.

- Bridging technical teams (engineers) with financial stakeholders (banks, sponsors).

These competencies became the backbone of Venture Global’s strategy.

Founding Venture Global (2013) product-market fit and architecture

In 2013, Robert Pender and Michael (Mike) Sabel co-founded Venture Global. Their complementary skillsets formed a natural founder embedding:

- Pender: project-finance attorney, expert in legal structure and contractual risk allocation.

- Sabel: capital markets, commercial strategy, and fundraising lead.

Their product thesis differed from that of major LNG incumbents:

- Modular, repeatable plants. Instead of building single, giant trains that take many years, Venture Global standardized modules that could be replicated across sites. This reduces first-unit lead time and enables learning-curve improvements.

- Faster permitting and construction cycles. The team prioritized rapid regulatory progress and compressed schedules.

- Long-term offtake deals. Secure sales contracts underwrite project debt and reassure lenders, a core requirement for project finance.

- Serial site development. Rather than a single flagship, the company pursued multiple sites in sequence, focusing on Louisiana projects in the Gulf region.

This strategy is optimized for speed, lower per-unit capital intensity, and the ability to scale through repeatable execution.

Scaling to IPO and rapid expansion change in observability

Venture Global’s growth used a combination of offtake contracts, project finance, and equity raises. The January 2026 IPO was a seminal event:

- Capital infusion: Converted private growth capital into public equity for expansion.

- Greater transparency: Public reporting obligations (10-Ks, 8-Ks, Form 4) made founder transactions and corporate disclosures visible to regulators, investors, and journalists.

- Market valuation: Founder paper wealth became visible and tied to day-to-day market dynamics, increasing the signal-to-noise ratio for media coverage.

With the IPO came both resources and scrutiny, a Common Pattern when private projects scale under public investor oversight.

Major projects & technical approach

Venture Global became associated with multiple Louisiana-based projects that operationalized the modular thesis:

- Calcasieu Pass: Early export terminal that served as proof of concept for modular design and sequential execution.

- Plaquemines LNG: A follow-up project designed to expand output using repeatable engineering modules.

- CP2 / CP3 / Delta: Subsequent phases to further scale export capacity.

Each of these projects pushed the same template: standardize a modular LNG train, compress procurement and construction timelines, and secure long-term capacity sales to underpin project finance.

Commercial & legal milestones

- IPO (Jan 2026): Public listing that crystallized founder value and increased disclosure obligations.

- Arbitrations & disputes: Claims from buyers about cargo allocation and delivery led to reputational and contractual stress.

- Offtake contracts: Long-dated offtake agreements were the creditor comfort for lenders and an essential commercial input for project finance.

Net worth & financial status

Estimating founder wealth from public market capitalization is noisy:

- Founder holdings are subject to dilution, lockups, and any secondary sales.

- Public reporting indicated multi-billion dollar paper valuations for founders at some 2026 price points, but such figures are volatile and depend on market prices.

- Income sources typically include founder equity, executive compensation, and prior professional earnings.

For live net-worth figures, check real-time finance trackers (Bloomberg, Forbes) and SEC filings for up-to-date holdings (S-1, Form 4).

The share-purchase controversy & political meetings timeline & mechanics

A central controversy in 2026 concerned founder share purchases and the timing of public meetings. Summarized mechanics:

- Reporting: The media reported that the co-founders purchased shares after market dips.

- Questions raised: Journalists and watchdogs examined whether purchase timing correlated with regulatory approvals, permits, or meetings with officials.

- Company position: Venture Global stated that insider trades complied with SEC rules and noted pre-approved trading arrangements when applicable.

- Public reaction: Optics matter, even legal trades can trigger investor suspicion when they coincide with regulatory milestones.

High-level compact timeline (as documented in public reporting)

- January 2026: IPO founder Ownership becomes public.

- March 2026: Media coverage surfaces about founder purchases following price dips.

- Spring–Late 2026: Investigative reporting, media scrutiny, and queries by lawmakers; company defends compliance with securities laws.

Why the controversy matters

From a governance lens, the controversy matters for three reasons:

- Optics: Insider buying usually signals confidence. But when purchases cluster near regulatory Developments, they attract heightened suspicion.

- Legal standard: Trading on material nonpublic information is prohibited. Company defenses typically rest on clean trading plans (e.g., 10b5-1) and timely Form 4 filings.

- Investor confidence: Even in the absence of an enforcement action, reputational damage can add volatility and increase cost of capital.

Arbitration & contract disputes: causes and consequences

Venture Global faced arbitration claims from some large buyers alleging allocation or delivery failures. Typical underlying drivers:

- Market tightness: In strained supply conditions, sellers may reallocate cargoes to higher-price buyers.

- Contract specifics: Force majeure language, allocation rules, and logistical constraints are determinative in disputes.

- Commercial remediation: Arbitration outcomes can affect recognized revenues, cash flows, and future contracting credibility.

Arbitration outcomes, settlement, award, or dismissal have direct implications for future sales, lender comfort, and the company’s reputation among large energy buyers.

Legal & regulatory context: the guardrails

Insider-trading basics

- Material nonpublic information (MNPI): Info that would influence a reasonable investor’s decision. Trading while possessing MNPI is illegal.

- 10b5-1 plans: Pre-arranged trading plans permitted under SEC rules; they provide a safe harbor when properly structured and executed.

- Disclosure obligations: Company insiders file Form 4 to disclose trades; public companies file 10-Ks and 8-Ks for material developments.

Energy approvals & permitting

LNG projects require a range of approvals that can materially affect project economics:

- Federal: DOE authorizations and FERC approvals are often critical.

- State & local: Environmental reviews, coastal permits, and local infrastructure approvals.

- Timing sensitivity: Changes to regulatory timelines or perceived preferential access to officials can be viewed as material events.

What this means for investors and the LNG market

For investors

- Upside: Modular builds can lower per-unit capex, accelerate first cash flows, and scale capacity quickly. Founder purchases sometimes signal alignment.

- Downside: Governance optics, potential litigation, and political scrutiny can increase volatility. Investors should monitor SEC filings (Form 4, 8-K, 10-K), arbitration dockets, and company disclosures.

For the LNG market

- Supply dynamics: Venture Global’s modular expansion added U.S. export capacity, influencing global LNG flows and pricing dynamics.

- Contracting friction: Arbitration with major buyers creates short-term operational noise and could affect counterparties’ risk perceptions.

- Sectoral learning: If modular builds prove broadly replicable, incumbents may adjust their product strategies, increasing competitive pressure.

Reputation, philanthropy & public profile

Compared to some billionaire founders, public records show limited philanthropic disclosure tied specifically to Pender. Coverage centers on corporate performance, contracts, and governance. Public profile is therefore professional rather than celebrity-centric.

The “Contract-First Founder” Model: Why Robert Pender’s Approach Is Different

Unlike many energy entrepreneurs who come from engineering or operations, Robert Pender represents a “contract-first” founder model—where legal structuring, risk allocation, and financing strategy shape the entire business from day one. This approach is especially powerful in LNG, where long-term agreements, lender protections, and regulatory approvals often matter as much as physical infrastructure.

At Venture Global, this mindset translated into a system where projects are not just built—they are pre-structured for financing, scalability, and repeatability. Instead of treating contracts as a final step, Pender’s model places them at the core of execution, helping the company move faster, secure funding more efficiently, and manage risk across multiple large-scale projects.

Comparison: Pender vs Sabel’s role decomposition

| Area | Robert Pender | Michael (Mike) Sabel |

| Background | Project-finance lawyer (contract structuring) | Capital markets & fundraising (commercial strategy) |

| Primary strength | Legal architecture, project development, and design | Fundraising, investor relations, public face |

| Public Role | Executive Co-Chairman behind-the-scenes deal design | Executive Co-Chairman / CEO — operational leadership and public interface |

| Controversy exposure | Subject of reporting on founder purchases & governance optics | Equally exposed; shares scrutiny as co-founder |

Pros & Cons

Pros

- Faster, modular builds reduce time-to-first-cash.

- Founder alignment via significant insider holdings can align incentives.

- Long-term offtake contracts provide debt underwriting for project finance.

Cons

- Governance optics can create reputational risk even without legal violation.

- Arbitration and contract disputes risk revenue disruption and client relationships.

- Market cycles (demand swings, oversupply) can compress margins.

Timeline of life & career events

- Pre-2010s: Project-finance attorney at major law firms (e.g., Hogan Lovells and peers).

- 2013: Co-founds Venture Global with Mike Sabel; adopts modular LNG build strategy.

- 2010s–early 2020s: Develops Calcasieu Pass, Plaquemines and other projects; secures offtake agreements.

- 2023–2024: Arbitration disputes arise with some buyers; execution continues.

- January 2026: Venture Global IPO — founder holdings gain public valuation.

- March–Late 2026: Media reporting and scrutiny over founder share purchases and meetings with officials; company asserts compliance.

Mini-case: modular build vs traditional build

Traditional single-train project

- One large train; longer lead time; higher single-project risk; higher per-unit capex.

Modular repeatable project

- Multiple smaller trains/modules; faster construction cycles (2–3 years per module); replicable design; lower per-unit capex.

Takeaway: The modular approach reduces time to first revenue, spreads risk across multiple execution steps, and benefits from design standardization.

FAQs

A: Robert Pender is co-founder and Executive Co-Chairman of Venture Global, a U.S. LNG exporter. He previously practiced as a project-finance attorney specializing in large energy and infrastructure deals. His strengths are in contract design, lender protections, and structuring long-term commercial deals that underpin capital projects.

A: Venture Global is known for a modular LNG approach: building repeatable export plants faster and at lower per-unit cost than many traditional projects. Key projects include Calcasieu Pass and Plaquemines. The company emphasized standardized module design, rapid permitting, and long-term offtake contracts.

A: Public reporting indicated co-founders purchased shares after market dips and that the timing raised questions. Venture Global stated that trades complied with SEC rules. For transaction specifics and exact dates, check the SEC EDGAR database (Form 4 filings) and company 8-Ks for contemporaneous disclosures.

A: Media and lawmakers queried the events in 2026. Whether the SEC initiated a formal investigation should be verified in the most recent public records; this article does not assert ongoing enforcement without official filings or agency statements.

A: Some major buyers alleged failure to deliver contracted cargoes or disputes over allocation priority. These cases typically hinge on contract wording (force majeure, allocation clauses), logistics, and market reallocation behavior. Arbitration outcomes affect revenue recognition risk and future counterparty trust.

Conclusion

Robert Pender’s career shows how legal expertise can become an industrial strategy when applied to a complex market like LNG. Venture Global’s modular build model helped the company scale quickly, but its public-market era has also exposed it to tougher questions about arbitration, insider trading optics, regulatory timing, and disclosure discipline. The 2025 IPO, the 2026 Edison Settlement, and the ongoing Plaquemines expansion show a business that is still growing, still controversial, and still very much shaped by the founder who helped design it. For readers and investors alike, the right lens is balanced: assess the operational upside, but read the filings, contracts, and court updates with equal care.