Chris Larsen’s Wealth & Charity

Chris Larsen, co-founder and longtime Ripple executive, is a leading fintech and crypto innovator. From launching digital lending at E-Loan and peer-to-peer services like Prosper to creating the XRP Ledger for cross-border payments, his work spans technology, management, and charitable projects. This article offers a detailed, NLP-style overview of his path: outlining major milestones, the 2020–2026 SEC lawsuit, wealth figures, notable gifts, and Ripple’s evolving role in financial markets. Whether you are a crypto investor, finance expert, or market analyst, this article presents a clear timeline and practical view of Larsen’s role in digital finance and banking.

Executive snapshot

- Full name: Christian A. Larsen (widely known as Chris Larsen).

- Born: 1960 (San Francisco Bay Area), approximately 65 years old in 2026.

- Education: Bachelor’s degree, San Francisco State University.

- Primary roles: Co-founder (E-Loan, Prosper, OpenCoin → Ripple Labs), longtime Ripple chairman.

- Known for: Early fintech entrepreneurship, co-founding Ripple, managing the XRP ledger, and a prominent SEC legal battle.

- Philanthropy: Large XRP donation to San Francisco State University (2019) plus other charitable contributions.

- Net worth: Values shift with XRP price; tracked continuously by Forbes.

Childhood & early life distilled

Chris Larsen grew up near the San Francisco Bay, immersed in a tech environment focused on easy-to-use finance tools. He earned a bachelor’s at San Francisco State University and later funded scholarships and campus initiatives, maintaining a giving connection. Early in his career, he worked to make lending and credit data more open and simple to access online, a consistent theme connecting E-Loan, Prosper, and Ripple: streamlining financial processes through software.

Career journey step-by-step

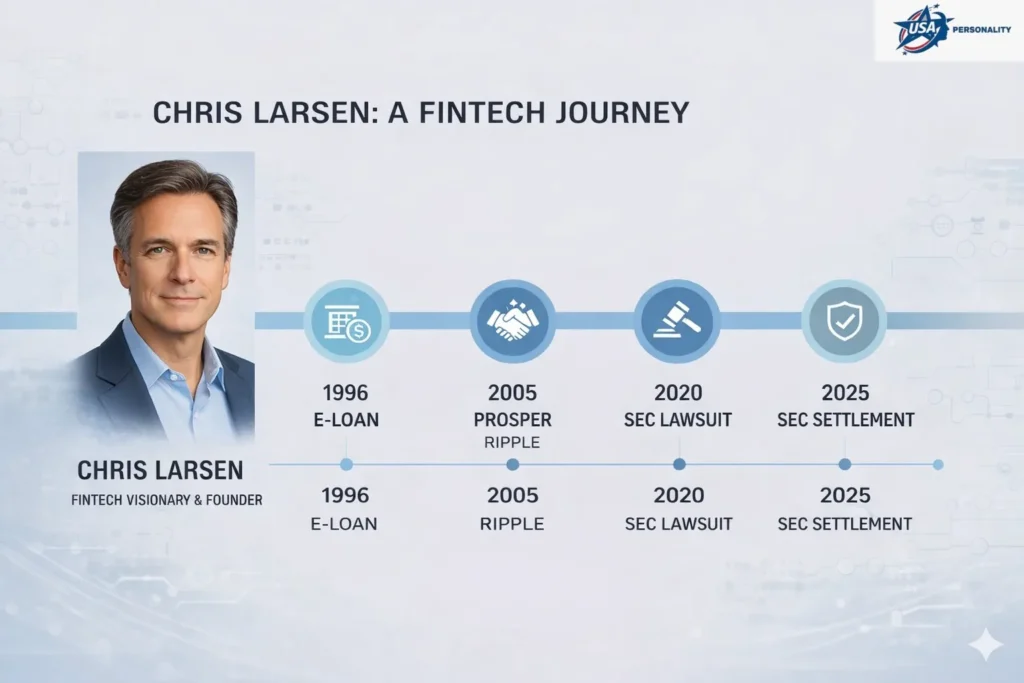

1996 E-Loan: an early mainstream online mortgage player

Larsen co-founded E-Loan in 1996. As an early mover to list pricing and credit information online, E-Loan made consumer finance data accessible and helped normalize online mortgage origination. That company provided Larsen with domain knowledge: regulated finance, consumer risk, underwriting flows, and product distribution.

2005 Prosper: peer-to-peer lending

In 2005 Larsen co-founded Prosper Marketplace, a pioneering peer-to-peer borrowing platform. Prosper matched retail investors to borrowers, accelerating the trend of marketplace lending but also exposing companies to sharper regulatory and underwriting scrutiny. Lessons from Prosper helped inform later decisions about tokens, liquidity, and disclosure.

2012 OpenCoin → Ripple Labs: payments & XRP ledger

OpenCoin, which later rebranded as Ripple Labs (commonly Ripple), launched with a design goal: a ledger and token (XRP) that reduces cross-border liquidity costs and accelerates settlement. Ripple’s public product narrative evolved from promoting XRP as a universal retail token to positioning enterprise software and liquidity services for banks and payment providers. The engineering team (including David Schwartz and others) built the XRP Ledger consensus protocol and validator network.

Major works & achievements

- E-Loan predicate: pioneer of online consumer lending and score transparency.

- Prosper predicate: early adopter of marketplace lending and risk-matching algorithms.

- Ripple/XRP Ledger predicate: developer of a near-real-time ledger and token for liquidity-on-demand; product emphasis on bank integrations and low-cost settlement.

These accomplishments map to different verb frames (invented, scaled, donated) and explain Larsen’s mixture of technical reputation and policy exposure.

The SEC litigation (2020–2026) an evidence-first timeline

This section is the most consequential for readers and markets. I present the timeline as an event sequence with citations to primary coverage and regulatory filings.

December 2020, the SEC filed suit

The U.S. Securities and Exchange Commission filed a civil enforcement action alleging that certain sales of XRP constituted unregistered securities offerings. This began a multi-year litigation and appeals process that became a signal case for token classification in the U.S. legal system.

2020–2023 partial rulings and legal parsing

By 2023, a federal judge ruled that programmatic XRP sales on public exchanges did not qualify as securities, but that some targeted institutional placements did meet the test for securities offerings. The decision created a bifurcated precedent: retail, exchange-based trading was treated differently from negotiated institutional transactions. This distinction influenced how exchanges and custodians treated XRP listings.

March–May 2026 settlement framework emerges

In early 2026, Ripple and the SEC agreed to a settlement framework and filed a settlement agreement with the SEC, which publicly described a reduced monetary resolution figure (reported in the press as $50 million at one point). That filing signaled de-escalation and an apparent move toward regulatory clarity, but such frameworks require judicial approval and may be subject to conditions.

June 2026 judge rebuffs joint motion to vacate prior findings

In June 2026, a U.S. district judge rejected a joint motion by the parties to vacate earlier findings and approve a reduced fine, saying that parties cannot easily erase final judicial rulings without extraordinary evidence. The judge’s caution demonstrated that negotiated settlements cannot retroactively erase judicial findings without the court’s independent evaluation.

June–August 2026 cross-appeals withdrawn, further resolution steps

Following judicial pushback, Ripple’s legal posture shifted: steps included withdrawing cross-appeals, adjusting settlement petitions, and responding to the court’s insistence on procedural safeguards. In August 2026 Reuters and other outlets reported that the SEC formally ended the case (with the $125M finding remaining in place, and injunction provisions on certain institutional sales retained), although press descriptions varied over timing and exact terms. The litigation’s procedural arc (complaint → partial rulings → settlement framework → judge’s rebuff → final motions and docket activity) left significant legal questions on record and clarified some and left others open.

Why the case matters, an NLP-style causal graph

From a systems perspective, the case is important because it changed the classification edges between tokens and securities law:

- Input nodes: token design & distribution metadata, public exchange listings, institutional sales documentation.

- Classifier output: securities vs non-securities. The court treated programmatic exchange sales and targeted institutional placements as different classes.

- Downstream effects: exchange listings, compliance requirements (Registration / Form S-1 equivalence), enforcement risk, market liquidity, token economics, and on-chain transfer monitoring.

In short, the case forced the U.S. market to move from a binary, label-only view of tokens toward a context-sensitive classifier that weighs distribution channel, purchaser expectation of profit, and contract-like arrangements.

Net worth & holdings: How to report responsibly

Why net-worth numbers swing (feature analysis)

Public Net Worth estimates for Larsen are highly sensitive to three features: (1) XRP market price, (2) visible on-chain transfers (large transfers change public perception and prompt revaluation), and (3) whether transfers were donations or sales (donations change ownership but may not be captured uniformly by trackers). Because Forbes and other outlets update rolling estimates based on token prices, any snapshot must be timestamped.

Public estimates & methodology cues

Forbes provides a real-time tracker that updates Larsen’s estimated net worth with market movements; publishers should cite the date/time for any figure. Avoid publishing an unsourced static number without a timestamp.

Philanthropy & public giving structured summary

- 2019 SFSU gift: Larsen, his wife Lyna Lam, and the Rippleworks Foundation donated $25M in XRP to San Francisco State University, one of the largest crypto-denominated university gifts reported at the time. This donation illustrates how digital assets can be used for major institutional philanthropy and raises operational questions for nonprofits about custody and conversion.

- Later civic giving: 2026 reporting flagged Larsen’s interest in funding local civic technology projects and a donation/pledge related to SFPD technology reports noted both support and privacy debate around such gifts. (Local press coverage summarized civic reaction.)

- Political contributions: Public filings and reporting show Larsen has used crypto and fiat to support political causes; these activities are increasingly visible as regulators and campaign finance systems adapt to digital assets.

Criticisms & controversies

- Concentration of supply: Large allocations of XRP to early insiders and the company have been criticized as creating Market Influence risk and raising decentralization concerns.

- Regulatory uncertainty: Protracted litigation made U.S. listing decisions and institutional adoption cautious for years.

- Institutional sale practices: The SEC’s focus on whether targeted, negotiated institutional sales required registration remains a central controversy.

- Public reception: Many retail holders celebrated the 2023 partial ruling that programmatic exchange sales were not securities, but the institutional-sale finding tempered market optimism and highlighted compliance risk.

A balanced narrative should present Ripple’s argument (that many XRP sales were not investment contracts, and that Ripple’s products serve enterprise needs) alongside judicial findings and regulatory reasoning.

Head-to-head: Ripple/XRP vs SWIFT vs Bitcoin quick comparison

| Feature / Metric | Ripple (XRP / RippleNet) | SWIFT (correspondent banking) | Bitcoin (BTC) |

| Primary use case | Institutional cross-border payments & on-demand liquidity | Interbank messaging & settlement coordination | Store of value; settlement layer |

| Settlement speed | Seconds (XRPL consensus) | Hours–days (bank processes) | Minutes–hours (network congestion) |

| Typical cost | Low per transaction (liquidity provisioning) | High (correspondent fees, nostro/vostro) | Variable; can be high for fast settlement |

| Regulatory maturity | Evolving; affected by SEC litigation | Mature, regulated banking networks | Evolving; global AML/KYC focus |

Net-worth & lifestyle

- Estimated net worth (example guidance): Always timestamp any estimate, e.g., “Estimate: $X as of YYYY-MM-DD (source: Forbes real-time tracker).” Forbes’ real-time tracker is a standard source for rolling estimates and should be embedded if possible.

- Income sources: Gains from token holdings (XRP), equity and compensation from earlier startups (E-Loan, Prosper), angel investments, and occasional donations that change visible holdings.

- Caveat: On-chain transfers can be misinterpreted (donation vs sale vs reallocation), so annotate events clearly when reporting.

Personal life

Chris Larsen is married to Lyna Lam. Media coverage emphasizes his ventures, charitable work, and regulatory activities, while other Personal Family details remain private. Include mentions of philanthropy and university connections where appropriate, but avoid guessing about his private life.

Lessons from Larsen’s career

- Problem framing matters: Larsen repeatedly targeted concrete payment and lending frictions to identify the pain, then engineered the minimum viable protocol/product to reduce it.

- Regulatory risk is a feature, not an accident: Fintech innovations will attract scrutiny; design with compliance in mind and plan for prolonged regulatory dialogues.

- New asset formats can enable new social behavior: Crypto donations show utility, but operational, tax and reputational issues follow.

Timeline compact

- 1960 Born (San Francisco area).

- 1996 Co-founds E-Loan.

- 2005 Co-founds Prosper.

- 2012 Co-founds OpenCoin / Ripple Labs.

- 2019 Donates $25M in XRP to San Francisco State University.

- 2020–2023 SEC enforcement action and partial rulings (public exchange vs institutional sale distinctions).

- 2024–2026 Settlement framework steps, judicial review, motions and case resolution reporting.

FAQs

A: Chris Larsen is an American entrepreneur, co-founder of E-Loan, Prosper, and Ripple. He is best known for his role at Ripple and for high-profile crypto-denominated philanthropy. (See Wikipedia and public profiles for background.)

A: The SEC sued Ripple (Dec 2020), alleging some XRP sales were unregistered securities. A 2023 ruling distinguished programmatic exchange sales (not securities) from certain institutional sales (securities). In 2026 Ripple and the SEC filed a settlement framework and settlement agreement; the judge later rebuffed attempts to vacate earlier findings or approve a heavily reduced fine without exceptional cause. Subsequent docket entries and press reporting described follow-on steps and the case’s procedural closure in 2026. Always consult court filings for precise legal language.

A: Estimates vary. Forbes and similar outlets publish rolling, timestamped estimates; values swing with XRP price moves and on-chain activity. Always timestamp any net-worth number and cite the source.

A: Yes — most notably a $25M XRP gift to San Francisco State University in 2019, and other philanthropic and political contributions reported publicly.

A: The settlement framework suggested regulatory progress, but judicial review limited what could be vacated or reduced. Exchanges and institutions will track final court orders closely; the legal distinction between programmatic public sales and targeted institutional placements is the main compliance takeaway.

Conclusion

Chris Larsen’s path connects problem-driven product design (E-Loan, Prosper, Ripple), real-world challenges of growing Financial Platforms, and regulatory pressures that innovation creates. The SEC lawsuit and 2026 settlement steps, with court review, changed legal rules for token distribution and shaped exchange and institutional compliance approaches. For writers: add dates, cite original sources, use structured markup, and rely on trusted references.