Introduction

Daniel Andrew “Andy” Beal is one of the most intriguing figures in modern finance: a private, disciplined billionaire who built a reputation by buying what others were forced to sell. Long before distressed debt became a mainstream topic, Beal was already applying a simple but Powerful Idea at scale: keep capital ready, buy assets at deep discounts, underwrite the collateral rather than the crowd’s mood, and wait for value to return.

That approach helped turn a modest start in real estate into a banking empire under Beal Financial and made him a recurring buyer in periods of market stress.What makes Beal stand out is not just the size of the fortune he built, but the consistency of the method behind it. He is also known for two unusual public footnotes: the Beal Conjecture prize, a million-dollar mathematics challenge, and his legendary ultra-high-stakes poker battles against some of the game’s best players. This article breaks down his background, business model, poker timeline, philanthropic angle, net worth, and the lessons readers can actually use.

Quick Facts

- Full name: Daniel Andrew “Andy” Beal.

- Born: November 29, 1952 (Age 72 in 2026).

- Main businesses: Beal Bank, Beal Bank USA, Beal Financial Corporation.

- Known for: Buying distressed loans & securities, ultra–high-stakes poker, and the Beal Conjecture prize.

- Reported profile (2026): Public profiles place his personal wealth in the multi-billion range; consolidated bank assets reported in the low-to-mid tens of billions across filings and profiles.

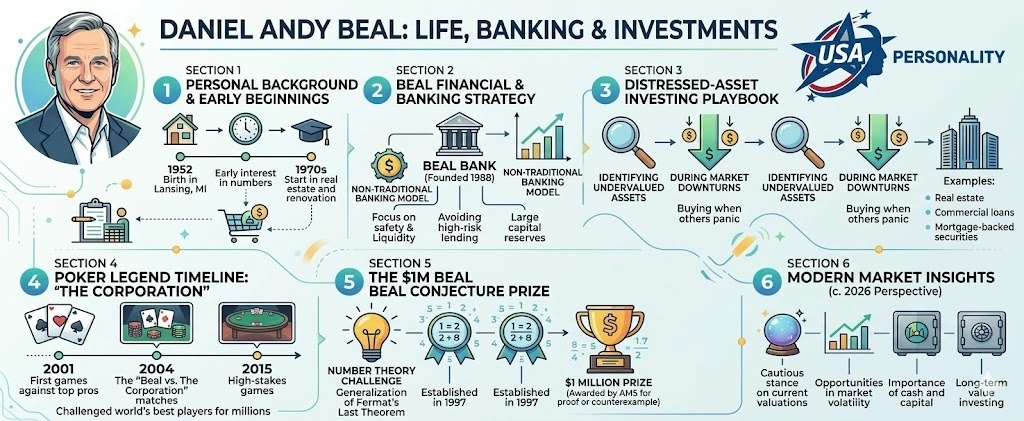

Childhood & Early Life

Andy Beal grew up in Lansing, Michigan. His upbringing was modest: his mother worked for the state and his father was an engineer. As a teenager and young adult Beal learned by doing buying a first house cheaply, fixing or re-leasing it, and using the proceeds to buy more properties. These early trades hardened three durable habits that inform his later strategy:

- Buy when things are cheap. Forced sales and distressed circumstances can create asymmetric payoff profiles.

- Add value or control costs. Renovation or tight management boosts realized returns.

- Hold strategically. Don’t sell into weakness; patience often captures the recovery.

These simple lessons capitalized by discipline and reinvestment, became the mental model he applied at a much larger scale once he moved into banking.

Career Journey From Local Real Estate to National Bank

Founding Beal Bank

In 1988, Beal consolidated his experience and capital into a bank-centric vehicle: Beal Bank, operating within Beal Financial Corporation. Instead of building a retail banking brand, he used the bank as a balance-sheet buyer: purchase distressed loans, nonperforming mortgages, and pools sold by regulators or failing institutions; then manage, restructure, or foreclose as appropriate until the underlying value was realized. Over time, this repeatable playbook let him acquire scale without the fanfare of public markets.

How Beal’s Banks Operate

At a practical level, Beal’s approach centers on a few operational pillars:

- Readiness of capital: Maintain liquidity and funding that allow rapid bidding when opportunities appear.

- Buy distressed assets: Whole-loan portfolios, FDIC/failed-bank pools, and sector-specific stress debt are typical targets.

- Collateral-first underwriting: Evaluate the recoverable value of collateral (real estate, aircraft, plants) rather than rely solely on market marks.

- Hold patiently: Use the bank’s balance sheet to collect income and wait for market recovery instead of forced resale.

This model reduces headline trading risk and captures the full recovery when markets normalize.

Core Investment Playbook

Core principles

- Buy distress, not attention. Seek forced sellers and avoid speculative market timing.

- Underwrite collateral, not short-term price moves. What can a loan fetch in a stressed liquidation or after restructuring? That is central.

- Hold to maturity when sensible. Capture coupon income and allow capital recovery over time.

- Scale by readiness. The ability to close large blocks is itself a competitive advantage; it creates opportunities unavailable to smaller buyers.

Case Studies Three Types of Beal Buys

Below are compact case studies that illustrate the playbook in action.

Case Study A: FDIC / Failed-bank loan pools

What he buys: Nonperforming loan Portfolios and whole loans sold by regulators or failed banks.

Why it fits: Forced sellers create steep discounts.

How Beal profits: Restructure, collect Payments, or foreclose, taking control of collateral that can be monetized or held for appreciation.

Real example: After the 2008 crisis and during later waves of stress, Beal’s companies purchased large portfolios sold by regulators and distressed institutions at material discounts and realized gains as credit markets recovered.

Case Study B: Sector-specific distressed debt

What he buys: Secured loans in troubled sectors (airlines, energy, aircraft financing).

Why it fits: Solid collateral reduces downside even if borrowers default.

How Beal profits: Wait for industry recovery, sell collateral, or restructure loans to sustainable terms. This category requires specialized underwriting to value unique collateral like aircraft or energy assets.

Case Study C: Opportunistic Treasuries & long bonds

What he buys: Large quantities of Treasuries or long-dated bonds during periods of attractive yields.

Why it fits: Treasuries are liquid and provide interest + optional capital appreciation if rates fall.

How Beal profits: Collect coupons, benefit from term premium, and realize mark-to-market gains when yields compress. Market filings and coverage have documented sizable bond holdings in recent years.

Table Quick Comparison of Beal’s Buy Types

| Type | What Beal Buys | Why it fits his playbook | Typical return driver |

| FDIC / failed-bank pools | Nonperforming loans, whole portfolios | Forced sales → big discounts | Loan recovery, restructuring, collateral |

| Sector distressed debt | Secured aircraft, energy loans | Collateral reduces tail risk | Recovery, liquidation, improved cash flows |

| Large bonds / Treasuries | Long-dated Treasuries & bonds | Scale + liquidity | Coupon + term premium + capital gains |

Scaling with Crises: The Counter-Cyclical Edge

Beal doesn’t loudly predict cycles; he prepares. The counter-cyclical edge requires:

- Discipline: Resist chasing crowded trades.

- Liquidity: Keep cash or funding to act when sellers are forced.

- Speed: Ability to bid, close, and take legal/operational control quickly.

When markets freeze or banks fail, Beal’s readiness converts into structural advantage. Reporting across cycles shows repeated involvement in regulator sales and bulk loan purchases.

The Andy Beal Poker Legend Timeline & Key Moments

Andy Beal’s poker story is an odd and humanizing counterpoint to his banking persona. In the early 2000s he sought out the world’s best heads-up players and engaged in a series of ultra–high-stakes matches against a group often called “The Corporation” (names reported in coverage include Phil Ivey, Barry Greenstein, Howard Lederer, Ted Forrest and others). The matches sometimes played at blinds and pots that ordinary players cannot fathom produced dramatic swings and became the subject of books and many articles. The saga did three things for Beal:

- Humanized him: It showed a billionaire willing to test himself in a skill-and-nerve game rather than sit passively behind a desk.

- Draw attention: The poker matches created narrative interest that nudged journalists to tell the story of a quiet distressed-asset buyer.

- Created folklore: The matches entered poker history as a rare collision between a private capital allocator and elite gamblers.

The Beal Conjecture Math & Philanthropy

Beyond banking and poker, Beal has made a Public Intellectual contribution: the Beal Conjecture, a generalization in number theory inspired by Fermat’s Last Theorem. Since the 1990s, he has offered an escalating monetary prize for a peer-reviewed proof or counterexample; the prize has been managed by the American Mathematical Society and stands at $1,000,000. This gift is a signal: Beal supports patient, intellectual problems where a single resolution advances human knowledge.

Beal’s 2026 Market Insights & Strategy Adaptations

Even decades into his career, Beal continues to adapt his approach to match evolving market conditions. In 2026, higher interest rates, geopolitical uncertainty, and regulatory changes are creating new distressed-asset opportunities. Sectors like commercial real estate in secondary markets, specialty lending (aircraft, shipping, industrial equipment), and energy-transition projects occasionally face forced sales. Beal’s strategy—maintaining liquidity, focusing on collateral, and patiently waiting for recovery—remains highly effective in these environments. Investors who emulate his disciplined approach can identify undervalued assets that others overlook, demonstrating that core principles of patience and readiness are evergreen, even as markets shift.

Net Worth & Financial Status

Public reporting places Beal among private billionaires whose wealth is closely tied to banking assets and privately held securities. Profiles from major outlets report consolidated assets for his banking group in the low tens of billions (reporting numbers vary by date and whether consolidated or per-bank figures are counted) and list his personal Net Worth in the multi-billion dollar range. Because Beal’s holdings are private and intentionally opaque, exact net-worth figures vary across outlets and times treat any single number as an estimate, not an audited truth.

Load-bearing citation (examples): Forbes and Bloomberg profiles summarizing Beal Financial’s scale and Beal’s billionaire status.

Pros & Cons

Pros

- Proven record of opportunistic purchases at discounts. Buying during forced sales has historically produced outsized returns for large buyers.

- Collateral focus reduces extreme downside versus pure market bets. Underwriting assets by recoverable value creates a defensive tilt.

- Scale & liquidity advantage. Large capital enables deals smaller buyers cannot touch.

Cons

- Requires a very large capital base. Retail Investors cannot replicate scale.

- Holding periods can be long. Long illiquidity increases risk if leverage or unexpected funding needs arise.

- Reputation noise risk. High public profile through poker or political donations can bring unwanted scrutiny.

What Investors Can Learn from Andrew Beal

- Prepare capital before the opportunity. Keep emergency capital so you can act during stress.

- Underwrite fundamentals and collateral. Invest where cash flows or recoverable collateral back the position.

- Be patient. Recovery often takes longer than headlines suggest; patience can capture the full recovery.

- Keep a low-noise footprint when useful. Operational secrecy can avoid tipping markets and reduce competitive pressure.

FAQs

A: Estimates vary. Profiles like Forbes and Bloomberg place him in the multi-billion range in 2026, with aggregated bank assets often reported in the tens of billions. Exact private holdings are not public.

A: He started in real estate, then moved into banking and opportunistic purchases of distressed loans and securities, buying when others were forced to sell and holding until value recovered.

A: Yes. He played ultra-high-stakes matches against top pros (often called “The Corporation”). The series had big swings, reported wins and losses, and became a well-known poker story.

A: Acquire underpriced or distressed loans and securities, underwrite based on collateral, hold the assets, and collect cash flows as markets recover.

A: Not directly, scale and capital access matter. But you can copy the principles: focus on underlying collateral, keep cash ready for opportunities, and think long term.

Conclusion

Daniel Andrew “Andy” Beal built a quiet but powerful financial career on a few durable principles: keep liquidity, buy forced sales at steep discounts, underwrite by recoverable collateral, and hold until value returns. That same discipline explains why he remains a compelling figure in both banking and poker, and why his philanthropy stands out in mathematics.

In 2026, his story still resonates because it is less about personality and more about process. Beal shows that disciplined readiness can outperform noise, and that patience can be a strategy, not just a virtue. Use that framework as a lens for evaluating distressed or asset-backed Opportunities, and the lessons from his career become immediately more useful.