Ramzi Musallam: Career, Deals & Worth

This detailed, segmented sketch of Ramzi M. Musallam draws a clear meaning outline of his work journey and investment approach. View the text like connected blocks (people, connections, date markers, transaction items, and review points) that viewers and writers can scan fast: his identity, how he built Veritas Capital into a sector-special private equity firm, the core strategy during his command, major holding outcomes, and how news outlets estimate his own fortune. Words stay easy yet borrow tech ideas like pieces, vectors, and purpose to simplify tricky company actions. If released, include direct-source hyperlinks (announcements, official profiles) and the date-line picture to raise trust and search ranking.

Quick facts

- Full name: Ramzi M. Musallam

- Current role: CEO & Managing Partner, Veritas Capital

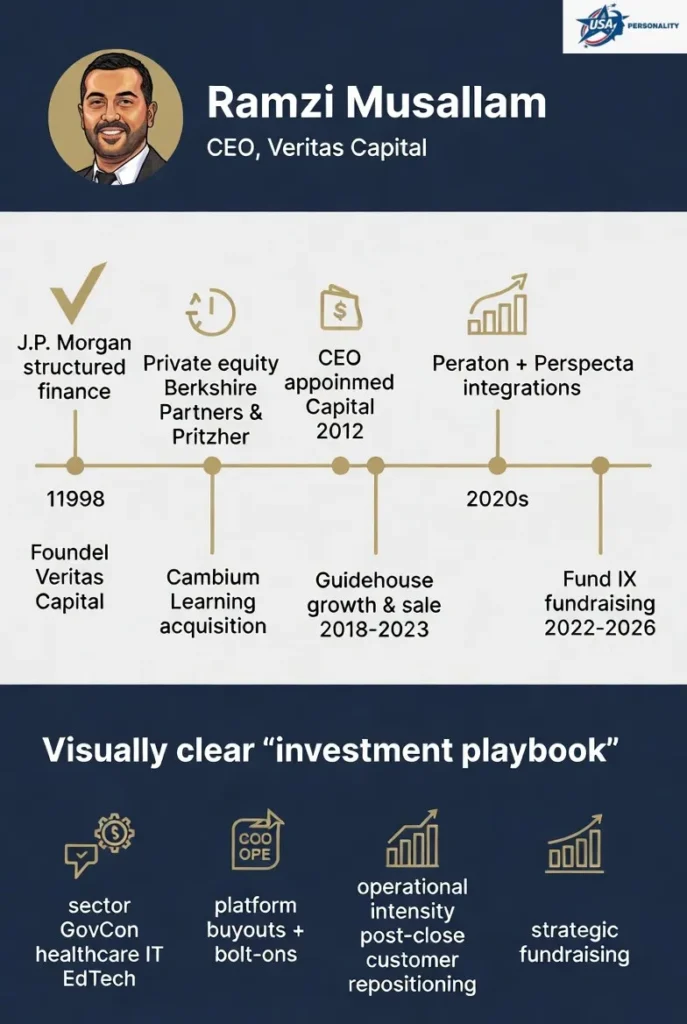

- Joined Veritas: Listed as a founding member of the firm’s first institutional fund (1998)

- Early career: Structured finance at J.P. Morgan; private equity roles at Berkshire Partners and Pritzker & Pritzker

- Industry focus: Government contracting (GovCon), healthcare IT, education technology (EdTech)

- Notable recognition: Frequent coverage in trade press and industry awards (e.g., Wash100; cited by press outlets such as Forbes and financial trade journals)

Childhood & early life, what’s public

Musallam maintains a private personal life; public records and profiles emphasize career and education rather than family background. The publicly available signal set centers on his technical training in structured finance, followed by a private-equity apprenticeship—data that helps explain his later emphasis on structured deals, carve-outs, and operational transformation in portfolio companies.

Career journey step-by-step growth

From structured finance to private equity

- J.P. Morgan Structured Finance: Early-career training that imparted expertise in capital structure, securitization, and complex contract design skills that translate to disciplined deal structuring and negotiation.

- Private equity stints at Berkshire Partners, Pritzker & Pritzker: These roles taught buyout execution, due diligence pipelines, and the governance frameworks that underpin operational value creation.

These formative positions created an embedding that blends technical dealcraft with operational turnaround instincts, an important neural motif that recurs in how he evaluates assets at Veritas.

Joining and building Veritas Capital

Musallam is recorded as a founding member of Veritas Capital’s first institutional fund in 1998. That founding-member status provided continuity and ownership context when the firm scaled its fundraising, sector specialization, and platform M&A strategies. He later became CEO & Managing Partner (reported in public profiles) and led a long program of platform builds, integrations, and fundraising.

Why this matters: Founding memory + CEO role = institutional continuity. In ML terms: a pre-trained model with fine-tuned domain layers, Veritas under Musallam keeps the core architecture but fine-tunes weights (operational playbooks) for each sector.

How Musallam built Veritas, the investment playbook

Below is a procedural decomposition of each step, which is a discrete operation Veritas frequently performs when evaluating, acquiring, and scaling assets.

Sector specialization

Hypothesis: Narrow domain focus yields higher signal-to-noise in sourcing and value creation.

Practice: Concentrate on sectors with long contracts, regulatory barriers, and mission-critical services (GovCon, healthcare IT, EdTech). This allows re-usable templates (operational checklists, KPI dashboards) and repeatable buyer-seller relationships.

Platform buyouts + bolt-ons

Operation: Acquire a platform (large, core asset), then perform bolt-on acquisitions to add capabilities, distribution, and revenue streams.

Example pattern: Build a consulting or services integrator by stitching together discrete capabilities, systems integration, managed services, and analytics under one governance stack.

Operational intensity after close

Operation: Post-close governance + operational playbook activation Leadership alignment, KPI redefinition, systems integration (ERP, CRM, security), and digital transformations. Veritas publicly touts operational work as essential to value creation.

Positioning to customers

Operation: Reposition companies as strategic partners rather than commodity vendors, improve contract structures, deepen program-level involvement, and create cross-sell pathways to reduce churn and increase lifetime value.

Fundraising as a strategic weapon

Operation: Raise large, patient funds to enable complex carve-outs and platform builds. A large fund allows Veritas to pay premium prices for strategic platforms and to underwrite multi-year integration plans.

Major works & achievements, notable deals and outcomes

Below is a concise selection of high-impact portfolio events and outcomes. This table is formatted to be copy-pastable into a CMS.

| Year | Company / Asset | Role & Outcome | Quick commentary |

| 2018–2023 | Guidehouse | Owned and grew Guidehouse; sale announced to Bain Capital (Dec 2023) | Platform build + consulting growth; a notable exit validating the playbook. |

| 2018 | Cambium Learning Group | Acquired Cambium; integration of Rosetta Stone and Lexia | EdTech consolidation: product-suite building and district-level sales expansion. |

| 2020s | Peraton & Perspecta | Integration to create larger GovCon integrator | M&A-led scale in federal systems integration and mission IT services. |

| 2010s–2020s | Health IT & Analytics (e.g., Cotiviti-related assets) | Investments and operational scaling in healthcare data & analytics | Focus on long-term, contract-based revenue streams in healthcare payment and analytics. |

| 2022–2026 | Fundraising Fund IX | Raised a large flagship fund (reported oversubscription) | Capital availability to pursue billion-dollar platforms and carve-outs. |

Net worth & financial status: How to present estimates

Net worth for private-equity principals is inherently estimation-driven because ownership stakes, carried interest, and unrealized fund values are not public. Public outlets occasionally publish estimates; the best publishing practice is clear sourcing and date-stamping any figure.

Why estimates vary

- Ownership percentage variance: Founder/partner stakes differ across funds and vintages.

- Carry & fee schedules: Carry crystallization occurs at exits, and fees dilute realized proceeds.

- Timing of exits: Market conditions and deal timing affect monetization value.

- Illiquid positions: Unrealized gains are modeled differently across outlets.

Publishing guideline: Quote the outlet and the date (e.g., “Forbes estimated $X as of [date]”) rather than printing an unsourced number.

Impact on GovCon, Healthcare & EdTech

GovCon consolidation

Veritas’ roll-ups create larger, integrated systems integrators capable of bidding for complex, multi-year federal programs. Consolidation changes competitive dynamics and the procurement landscape.

Healthcare IT

Investing in healthcare data platforms (analytics, claims, outcomes) shifts focus toward value-based care enablement assets that can supply analytics and payment integrity capabilities to payers and providers.

EdTech

Through Cambium and bolt-ons, Veritas demonstrated the transferability of the platform playbook assembling content, assessment, and language solutions into a single product stack appealing to districts and international markets.

Balanced critiques & controversies

A credible profile presents both sides. Below are common criticisms and the frequent public responses.

Criticisms often raised

- Consolidation concerns: Roll-ups may reduce competition and create pricing power for essential services.

- Private equity incentives vs. public mission: When companies serve public programs or schools, profit motives may conflict with mission delivery or service quality.

- Transparency & public interest: Ownership changes in firms serving taxpayers invite scrutiny around continuity, cost, and performance.

Veritas’s and Musallam’s public responses

- Operational investment framing: Veritas emphasizes investments in systems, personnel, and long-term product development, portraying acquisitions as capacity-building rather than extraction.

- Customer continuity: The firm highlights continuity planning and contract stewardship when transitioning ownership of mission-critical businesses.

Editorial guidance: Pair firm statements with independent reporting (press releases and coverage) to let readers draw their own conclusions. Use facts: contract renewals, program performance metrics, and independent audits where available.

Personal life

Musallam is a private individual. Public reporting typically lists education (including an MBA from Booth referenced in profiles) and career milestones rather than personal details. Ethical coverage should avoid unverified personal claims and focus on verified professional facts and primary sources.

Motivational lessons that leaders can learn from Musallam

Below are concise, transferable lessons you can apply in leadership or investing contexts:

- Pick a defensible niche and master it. Deep domain knowledge produces repeatable pipelines and better due diligence.

- Operational focus after purchase matters. Financing is necessary, but insufficient product, people, and systems matter for durable value.

- Fundraising is a strategy. Large, patient capital opens strategic options and the ability to underwrite complex integrations.

- Frame acquisitions as stewardship when public customers are involved. Clear communication and mission alignment reduce stakeholder friction.

Year-by-year timeline

- 1990s: J.P. Morgan Structured Finance (technical training).

- Late 1990s: Private equity roles at Berkshire Partners and Pritzker & Pritzker.

- 1998: Founding member of Veritas’ first institutional fund.

- 2012: Named CEO & Managing Partner, Veritas Capital.

- 2018: Veritas acquires Cambium Learning Group.

- 2018–2023: Veritas grows Guidehouse and completes a sale (announced to Bain Capital Dec 2023).

- 2020s: Peraton + Perspecta integrations expand GovCon footprint.

- 2022–2026: Continued fundraising, including a large flagship Fund.

Table Selected deal features, rationale & outcome

| Company | Why Veritas bought it | Actions taken | Outcome |

| Cambium Learning | EdTech reach & product mix | Added Rosetta Stone & Lexia | Larger digital learning group |

| Guidehouse | Consulting platform, recurring revenue | Growth + M&A | Exit to Bain Capital (reported $5.3B) |

| Peraton | Build large GovCon integrator | Merged Perspecta & assets | Larger federal market share |

Pros & Cons

Pros

- Deep sector expertise improves deal selection.

- Strong fundraising allows big platform deals.

- Operational focus can improve product and customer continuity.

Cons

- Market concentration can concern policymakers and customers.

- Private-equity ownership of public-service suppliers raises incentive questions.

- Large platforms may face regulatory or antitrust review.

FAQs

A: He is the CEO & Managing Partner of Veritas Capital, a private equity firm that invests in companies serving government, healthcare, and education.

A: He started at J.P. Morgan in structured finance, worked at Berkshire Partners and Pritzker & Pritzker, then joined Veritas as a founding member of its first institutional fund. He became CEO in 2012.

A: Cambium Learning Group (edtech), Guidehouse (consulting), Peraton (government integrator), plus investments in healthcare IT firms.

A: Estimates vary. Use specific reports (Forbes, Bloomberg) and date them, e.g., “Forbes reported X as of [date].” The exact value is private and changes with exits.

A: He has been recognized multiple times by GovCon industry awards, including the Wash100.

Conclusion

Ramzi Musallam has presided over a repeatable, sector-led private-equity approach: identify sectors with durable demand signals, acquire or assemble platforms, deploy bolt-on acquisitions to fill capability gaps, and apply concentrated operational effort after close. This architecture, akin to a modular ML pipeline with reusable components, has produced concrete outcomes: platform expansion in consulting and GovCon, targeted roll-ups, and significant fundraises that enable large carve-outs. Those results explain industry recognition and repeated coverage. However, the model also invites scrutiny: assets often deliver essential public services or education products, and consolidation raises policy questions about competition and stewardship. Balanced coverage should therefore combine the firm’s statements about stewardship and investment in operations with independent verification about contract continuity, program performance, and effects on competition. For publishers, adding primary-source links, an embedded Timeline, and downloadable resources will boost trust and time-on-page, helpful both to readers and search engines.