Introduction

Orlando Bravo is a key figure in modern private investing. He helped expand a small equity group into Thoma Bravo, one of the world’s most active and focused firms for acquiring, enhancing, and scaling business software companies. Bravo’s method is practical and repeatable: target software with subscription income, identify operational weaknesses quickly, follow a fixed management plan, add supporting companies, and then either sell at higher prices or restructure to secure profits.

This guide explains who Orlando Bravo is, how Thoma Bravo’s software-first approach works in practice, the key deals that shaped the firm, Bravo’s charity efforts for Puerto Rico, the main dangers and criticisms the firm faces (including public events like SolarWinds), and the trends to watch as AI changes business software in 2026. The content uses clear headings and simple words so it’s easy to read, reuse, or optimize for search.

Quick facts

- Full name: Orlando Bravo

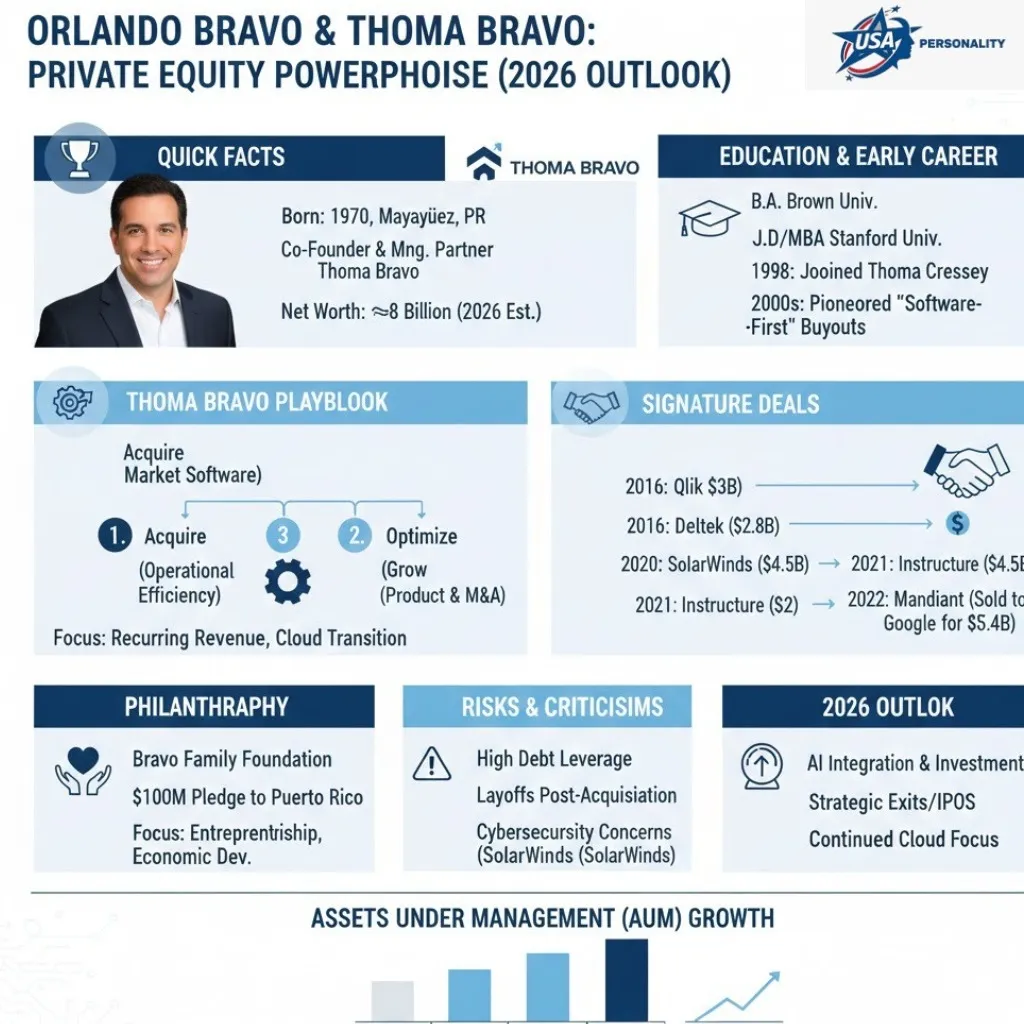

- Born: 1970, Mayagüez, Puerto Rico.

- Education: Brown University (BA); Stanford Law School (JD); Stanford GSB (MBA).

- Role: Co-founder & Managing Partner, Thoma Bravo.

- Firm AUM (mid-2026): Public figures reported in the range of roughly $160–$181 billion.

- Philanthropy: Founder of the Bravo Family Foundation; personally committed $100M to Puerto Rico entrepreneurship (announced 2019).

Childhood & early life

Orlando Bravo was raised in Mayagüez, Puerto Rico, in 1970. His early years on the island make part of his public story: family, local ties, and an early work habit that shaped how he views duty and success. Those roots also guide his charity focus now; Bravo has often highlighted giving back to Puerto Rico and helping local business growth as part of a long-term development plan.

Education & early career, a clear foundation

Bravo mixed arts study and practical learning: a college degree from Brown University, followed by both a JD and an MBA from Stanford (Law School and Business School). That unusual blend of law and business lessons gives him skill across deal setup, rules complexity, and the tactical market levers that matter after a purchase.

Early in his work, he served in banking and private capital posts where he gained deal know-how. Those first years taught him how to read financial reports, bargain protective clauses, and plan incentive systems — all abilities later reused at scale once he helped develop Thoma Bravo’s software focus.

The formation of Thoma Bravo and the software specialization

Thoma Bravo evolved from earlier business structures into a focused, sector-centric firm. Under Bravo’s influence, the firm deliberately narrowed to enterprise software and tech-enabled services. Why that focus worked:

- Recurring revenue (subscriptions, maintenance) gives predictability.

- High gross margins mean operational improvements translate quickly to cash flow.

- Product and go-to-market fixes can materially change growth trajectories in months, not years.

- Consolidation opportunities: many vertical software markets are fragmented — buy a platform and add tuck-ins to expand share.

This sector focus enabled Thoma Bravo to create standardized operating teams, repeatable playbooks, and a deal pipeline where the firm’s in-house knowledge generated a competitive edge. Over time, the firm moved from doing dozens of software deals to hundreds, building institutional muscle and fundraising scale.

The Thoma Bravo playbook on how they actually create value

Thoma Bravo’s value creation process reads like an operations manual. It’s simple to state but rigorous to execute. Below is a distilled, publishable version of the playbook and a practical 30/60/90 checklist.

Core pillars

- Sector focus: Enterprise software and tech-enabled services.

- Repeatable ops: Standardized post-close playbooks (pricing, retention, sales efficiency).

- Bolt-on consolidation: Acquire a platform, then tuck in smaller assets to expand product breadth and market penetration.

- Data & KPIs: Standardize ARR, gross retention, net dollar retention, CAC payback and LTV.

- Active governance: Tight partnership with management and strong board oversight.

Signature deals mini case studies

These deals illustrate the pattern: identify a software or software-adjacent business with recurring revenue, buy it, operate it, consolidate or improve product/sales, then exit or recapitalize.

Qlik analytics & take-private (2016)

- Year: 2016 (take-private).

- Deal worth: Around $3.0 billion.

- What occurred: Thoma Bravo agreed to buy Qlik in 2016 and made the company private with a deal set at roughly $30.50 per share. The firm later worked on recapitalizations and share sales as part of a longer-term value plan.

Deltek niche enterprise ERP (2012 → sold 2016)

- Year: Acquired 2012 (take-private), sold 2016.

- Buy price: ~ $1.1 billion.

- Exit: Sold to Roper Technologies for about $2.8 billion in 2016.

- Play: Focused investment in product and go-to-market, and a series of tuck-ins that expanded market penetration.

SolarWinds large platform, governance questions (2015–2016)

- Year: Thoma Bravo (with Silver Lake) took SolarWinds private in 2015–16 for about $4.5 billion.

- Why it matters: SolarWinds later became the centre of one of the most consequential supply-chain cyberattacks, disclosed in late 2020. The incident raised public questions about governance, security culture, and whether private-equity ownership models adequately prioritize cybersecurity Investments across software portfolio companies. The breach involving the SUNBURST backdoor and impacting thousands of customers, including U.S. federal agencies,s remains a landmark case study for PE governance risk.

Instructure EdTech (2019 → exit/recap)

- Year: Acquired in 2019; Thoma Bravo later restructured and partially exited via public listing and sales; KKR agreed to acquire Instructure in 2024 in a deal valued at about $4.8B. The path shows how PE can reposition an asset through product investment and M&A before a strategic sale.

Philanthropy, Bravo Family Foundation & Puerto Rico

Orlando Bravo’s charity work is a clear part of his personal story. The Bravo Family Foundation centers on startups, learning, and restoring economic strength in Puerto Rico. In May 2019, Bravo personally gave $100 million to the foundation to back entrepreneurship, ecosystem growth, and long-term local development on the island. The foundation also offered fast relief after Hurricane Maria and has funded accelerators, grants, and mentoring programs aimed at building lasting local businesses.

A main design idea: the foundation often mixes money with practical help, networks, and guidance — copying the capital plus operations method used at Thoma Bravo, but applied to community and local ecosystem growth.

Risks, criticisms & industry headwinds

Specialization and scale bring advantages and unique risks. Here are the main areas of scrutiny and macro exposures for Bravo and Thoma Bravo.

Leverage & macro risk

Private equity buyouts typically use debt. In a rising-rate environment, servicing that debt becomes pricier and can compress operating flexibility. Heavily leveraged transactions can struggle if revenue growth stalls.

Concentration risk

Thoma Bravo’s deep focus on enterprise software is a strength in good times and a vulnerability if software multiples compress or enterprise IT spending slows. Concentration magnifies sector cycles.

Governance & cyber risk

High-profile events like the SolarWinds supply chain breach highlight management and safety standards for PE-owned software companies. The SolarWinds example showed how a hacked update can create worldwide effects and how questions about safety methods can become reputational and legal dangers for owners.

Public perception & ESG

Private investing faces review on work effects, price shifts, and how control influences long-term service standards for clients. These discussions guide rule-making and investor talks about proper PE conduct.

What’s next for Bravo & Thoma Bravo in 2026

Several themes are likely to shape the firm’s trajectory in 2026:

AI & generative AI

Enterprise software will keep integrating AI features. Thoma Bravo will likely prioritize acquisitions that add AI capabilities, infrastructure, or security solutions. AI is both an offense (new product value) and a defense (new risk vector).

Fundraising & AUM growth

Large fund closures signal investor confidence. As of mid-2026, the firm publicly cited AUM figures near the $160–$181B range; new funds and credit pools will remain critical to how aggressively the firm can bid on massive platform deals.

Exit strategy preferences

Given market volatility, PE firms might prefer recapitalizations, minority stake sales, and strategic partnerships over timing risky IPO windows. The Qlik recapitalizations and minority stake sales are examples of flexible exit approaches.

Security & governance spotlight

After events like SolarWinds, expect more careful review on cyber protection during deal steps and a higher standard for continued safety spending in portfolio firms.

Lessons for founders & investors: practical takeaways

Whether you’re a founder or an investor, Bravo’s playbook offers concrete lessons:

- Specialize to scale: Deep sector knowledge compounds across deals. If you can become the go-to expert in a niche, you get better deal flow, better pricing, and repeatable operating playbooks.

- Pair capital with operations: Cash plus operational guidance is far more valuable than capital alone. Standardized templates accelerate time to value.

- Prioritize governance and security: Technical debt and governance gaps are often the weakest link after an acquisition. Build remediation plans early.

- Think ecosystem, not just exits: Bravo’s philanthropy connects capital to Local Ecosystems, apply the same mindset to customers and partners.

- Be flexible on exits: Market conditions change. Have multiple exit paths sale, recap, minority stake, or eventual IPO, and design company economics to be robust across options.

Timeline of key life & firm events

| Year | Milestone |

| 1970 | Born in Mayagüez, Puerto Rico. |

| 1992 | Graduated from Brown University (BA). |

| Late 1990s | Completed Stanford JD & MBA. |

| 2012 | Thoma Bravo acquires Deltek (~$1.1B). |

| 2015–2016 | SolarWinds acquisition (~$4.5B). |

| 2016 | Qlik take-private (~$3.0B). |

| 2019 | Pledged $100M to Bravo Family Foundation (Puerto Rico). |

| 2024–2026 | Firm publicly cited AUM figures in the ~$160–181B range. |

Table Signature deals snapshot

| Deal | Sector | Thoma Bravo action | Outcome / Status |

| Qlik | Data analytics | Take-private 2016 (~$3B) | Recapitalizations and minority stake sales. |

| Deltek | Project ERP | Take-private 2012 ($1.1B) | Sold to Roper in 2016 for ~$2.8B. |

| SolarWinds | IT Management | Take-private 2015–16 (~$4.5B) | Later became the centre of a major cybersecurity incident. |

| Instructure | EdTech LMS | Acquired 2019 | Sold/recapitalized; KKR deal ~$4.8B announced. |

Pros & Cons

Pros

- Specialist expertise in enterprise software.

- Repeatable operating playbook that scales across deals.

- Large AUM gives deal flexibility and access to big transactions.

- Targeted philanthropy that links capital and operational support to ecosystem development.

Cons

- Concentration in one sector (software) raises exposure to sector slowdowns.

- Leverage used in buyouts increases sensitivity to interest rates.

- Public & regulatory scrutiny accelerates after incidents like SolarWinds; reputational risk matters.

FAQs

A: He is a co-founder and the firm’s leading partner. He helped form its software focus.

A: In May 2019, he declared a personal pledge of $100 million to the Bravo Family Foundation to back entrepreneurship and growth in Puerto Rico.

A: Business software and tech-based services, especially firms with subscription income and strong client retention.

A: Yes. For instance, SolarWinds was taken private in 2016 and later became involved in a major cyber attack, which raised questions about management in PE-owned software companies.

Conclusion

Orlando Bravo is an important person in modern private investing. He helped grow Thoma Bravo into one of the most strong, software-focused backers worldwide by mixing sector focus with a strict operational plan. The firm’s major deals from Deltek to Qlik to SolarWinds and Instructure show both the benefits and the dangers of the model: when product, price, marketing, and bolt-on acquisitions are done well, value can form quickly; when governance or safety holes emerge, reputational danger and rule review can follow.

Bravo’s charity work shows how money and networks can be aimed at local economic issues, especially in Puerto Rico. As AI and security reshape business software in 2026, Thoma Bravo’s strengths — deep sector know-how, repeatable operations, and plenty of capital — will stay useful, but so will the need for stronger governance and safety checks. For founders and investors, the main lessons are to specialize, link money with operational steps, and keep clients and Security at the heart of strategy.