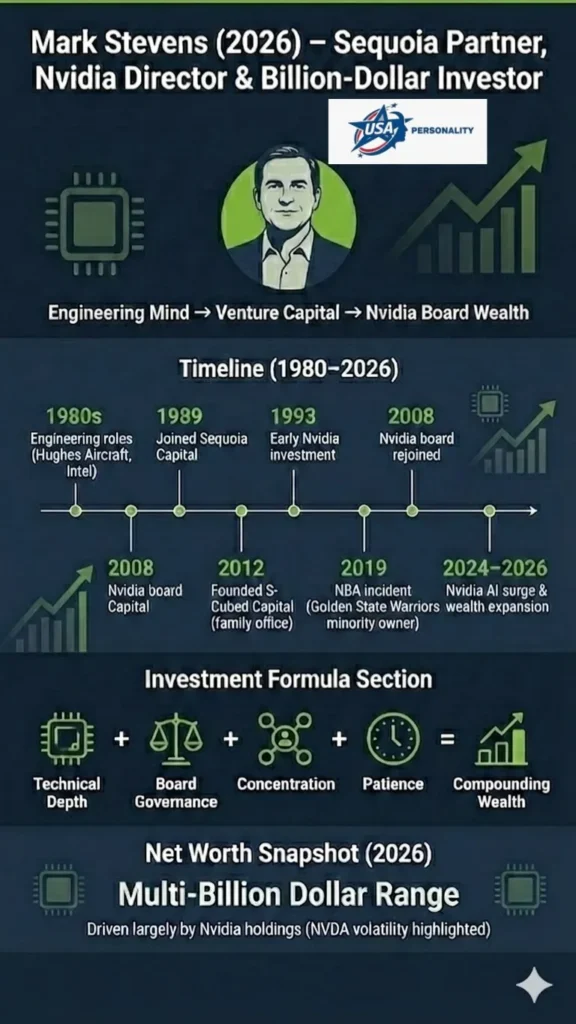

Mark A. Stevens: Worth & Career

Mark A. Stevens stands as a low-profile yet powerful Silicon Valley capital allocator whose blend of engineering background, hands-on leadership, and long-term oversight created one of the classic venture triumphs over the last thirty years. Following an engineering career at Hughes and Intel, Stevens joined as a partner at Sequoia Capital, concentrating on chip technology, computing platforms, and core systems prior to launching his family investment firm, S-Cubed Capital, during the 2010s. His early conviction in NVIDIA, coupled with board service and years of patient holding, is the clearest single driver of public estimates of his 2026 wealth. This profile walks through Stevens’s upbringing, education, Sequoia years, the Nvidia thesis, S-Cubed’s family-office playbook, his investment rules, the public reputation risk from the 2019 NBA incident, and practical checklists founders can use when preparing for a Stevens-style, technically fluent director investor.

Quick facts

- Full name: Mark Anthony Stevens.

- Born: February 17, 1960 (Los Angeles County, California).

- Education: USC (engineering degrees), Harvard Business School (MBA).

- Current role (2026): Managing Partner, S-Cubed Capital (family office).

- Known for: Early Nvidia investor and long-time director; former Sequoia partner; founder of S-Cubed Capital.

- Public net-worth (2026 est.): Multiple public estimates place him in the multi-billion range, driven largely by Nvidia holdings and changes in NVDA’s share price. (See Sources & notes.)

Childhood, education, and early technical grounding

Mark Stevens grew up in Southern California. From an early age, he gravitated to engineering and systems thinking interests that led him to the University of Southern California for undergraduate and graduate engineering work and later to Harvard Business School for an MBA. Stevens’s early professional stops at Hughes Aircraft and Intel combined hands-on technical work with customer-facing roles. That mix of engineering fluency plus sales/marketing exposure is a throughline of his later approach: an investor who can read technical roadmaps and also judge whether the product solves a real customer problem.

Career journey step by step

1980s from engineer to investor mindset

Stevens’s earliest roles gave him credibility with founders and product teams. At Intel he worked in technical sales and marketing; the experience of translating complex chip capabilities into product value is precisely the kind of practical domain expertise that later allowed him to spot winners in semiconductors and systems. That practical grounding distinguishes him from investors who are purely financial first and technical second.

1989–2012 Sequoia Capital: specialization and influence

Stevens joined Sequoia in 1989 and became a partner in the early 1990s. At Sequoia, he concentrated on semiconductors, infrastructure, and systems software, a focused remit that plays to his strengths. Over two decades, he participated in diligence, board work, and portfolio construction at one of the preeminent venture firms. Inside Sequoia’s partnership, specialists like Stevens often function as the technical anchor on chip and systems bets, bringing detailed product and architecture judgment to investment debates.

2012 → present S-Cubed Capital: the family office pivot

Around 2012, Stevens transitioned from Sequoia Partnership to running S-Cubed Capital, his family office. The change matters: family offices can hold concentrated stakes longer, accept private placement and secondary opportunities, and take board positions without the same calendar of fund lives and limited-partner pressures. Stevens’s move is a classic example of a senior VC taking family capital to pursue longer, more concentrated positions with closer governance.

Signature deals & the Nvidia story, why Nvidia is the headline example

Early investment thesis: GPUs beyond gaming

NVIDIA’s earliest market was high-throughput graphics for gaming and professional visualization. Investors who saw GPUs as purely a gaming play missed the bigger architectural truth: GPUs perform massive parallel matrix and vector math extremely efficiently. When machine learning and neural networks became mainstream workloads, GPUs were ideally suited to the dense linear algebra and parallelism those workloads require. Stevens’s technical background let him read that architectural mismatch between market perception (graphics only) and underlying capability (general compute for ML). That insight underpins his early conviction.

Board role + governance = optionality and influence

Stevens did not limit himself to a passive position. He served on Nvidia’s board during critical phases, giving him direct visibility on product roadmap, capital allocation, and executive decisions. Board membership is a different form of involvement than owning shares alone: it gives the investor an active seat at governance, the ability to ask specific strategic questions, and a view into management integrity and technical execution. That combination of technical thesis + board seat + patience is why Nvidia became the clearest single driver of Stevens’s public wealth.

Outcomes and compounding

As Nvidia expanded from gaming GPUs into data-center AI compute, its valuation rose dramatically. Early concentrated investors with board insight and a long hold period saw outsized returns. Public articles and billionaire indices have repeatedly pointed to Nvidia as a primary driver of Stevens’s multi-billion valuation in the mid-2020s. (See Sources & Notes for numbers and caveats.)

Other Sequoia-era successes and the value of domain focus

While Nvidia is the marquee win, Stevens’s career at Sequoia included many semiconductor and systems investments. The pattern is consistent: deep technical fluency lets an investor ask harder product questions, detect subtle architectural advantages, and identify teams that understand tradeoffs most founders never articulate clearly. Within a broad partnership team, those technologists often push through the bets that later look obvious in hindsight.

S-Cubed Capital: the family office playbook

S-Cubed Capital illustrates how a founder-turned-partner can use family capital differently than an institutional fund:

- Concentration: Family offices can take larger percentage positions.

- Time horizon: No fixed fund life means patient compounders can hold stakes for decades.

- Governance focus: Directors and advisors are often drawn into active governance.

- Flexible instruments: Secondary purchases, private placements, and public purchases are all possible.

This vehicle suits investors who prioritize influence and long-term value creation over short-term liquidity events.

Mark Stevens’s investment strategy has practical, replicable rules

Below are distilled rules that capture Stevens’s playbook. They’re stated plainly and are actionable for founders and investors:

- Specialize in a technical domain. Invest where you can judge product roadmaps and microarchitectural choices yourself. Domain fluency converts signal into conviction.

- Prefer board seats when conviction is high. Governance brings both influence and information asymmetry.

- Concentrate where conviction is highest. A few large bets can outperform many modest ones, but accept the volatility that comes with concentration.

- Work with founders, not above them. Technical help plus operational humility wins trust and alignment.

- Be patient. Some compounders take a decade or more to become visible winners.

How founders should talk to Stevens-style investors: a practical checklist

If you want to attract an Investor who thinks like Stevens, prepare to demonstrate the following clearly:

- Technical roadmap in plain language. Show milestones, scaling limits, and latency/throughput tradeoffs.

- Unit economics and margin trajectory. Explain how scaling improves gross margins and reduces per-unit cost.

- Honest risk map. Be candid about failure modes and mitigation. Investors respect realism.

- Board readiness. Describe the governance structure you want and the specific help a technical director could add.

- Long-term orientation. Highlight why short PR moves aren’t substitutes for durable product advantages.

Philanthropy, sports ownership, and public persona

Stevens and his wife are known donors to USC and have taken roles that bridge philanthropy and institutional influence (trustee roles, advisory boards). He is also a minority owner of the Golden State Warriors a higher-visibility public role that brought both prestige and reputational risk. His USC philanthropic ties are well documented and consistent with the typical pattern of technologists and VCs supporting engineering and research initiatives at their alma mater.

The 2019 NBA incident: what happened and reputational fallout

In June 2019, during Game 3 of the NBA Finals, Mark Stevens shoved Toronto Raptors guard Kyle Lowry after Lowry leapt into the front row to chase a loose ball. The video captured the push and the subsequent verbal exchange. The NBA investigated and fined Stevens $500,000 and banned him from NBA games and team events for one year. The incident became widely reported and generated public discussion about owner conduct and the reputational exposures public figures accept by taking visible team roles. Stevens issued apologies and reportedly reached out to Lowry to apologize directly.

Reputation lesson: sport ownership increases public visibility and amplifies non-investment behavior. For investors considering visible roles outside finance, the tradeoff between profile and reputational risk is real and measurable.

Net worth & holdings

Important caveats before numbers: public net-worth estimates are snapshots derived from public filings, board disclosures, insider tables, and public market valuations. Family-office holdings may be partially private and are often estimated. When NVDA’s share price moves meaningfully, the headline net-worth estimates tied to insiders will swing by billions. Treat any single number as an approximate, date-stamped estimate rather than a precise ledger.

Simplified holdings overview

- NVIDIA (NVDA): Early investor, longtime director, principal public source of net-worth uplift.

- S-Cubed public positions: Family office stakes traded publicly and privately.

- Private board roles: Active governance in semiconductor and systems firms.

- Golden State Warriors: Minor Ownership stake, public visibility, and non-financial exposure.

Public outlets in 2024–2026 placed Stevens’s net worth in the multi-billion range, often citing NVDA holdings as the primary driver; different outlets use different methods (insider holdings × market price, filings, reported sales). See Bloomberg, Forbes, and other trackers for date-specific snapshots.

Timeline of life events

- 1960: Born (February 17).

- 1981–1984 (approx.): USC degrees (BS/MS in engineering).

- 1987 (approx.): Harvard Business School (MBA).

- 1989: Joined Sequoia Capital.

- 1993: Early Nvidia investment and board involvement begin.

- 2001: Joined USC Board of Trustees (serving in various roles).

- 2008: Rejoined the Nvidia board after prior service (reported board periods).

- 2012: Shift to S-Cubed Capital (family office) approximate.

- 2013: Joined Golden State Warriors ownership group (investor).

- 2019: NBA incident (shoved Kyle Lowry) $500,000 fine and one-year ban.

- 2024–25: Nvidia’s AI surge elevates valuations of long-term insiders and board members.

Pros & Cons

Pros

- Deep technical domain knowledge in semiconductors and systems.

- Track record of early identification and patient board stewardship.

- Institutional philanthropy and university influence (USC).

Cons

- Concentration risk: Large, concentrated holdings (especially in one public company) create headline net-worth volatility.

- Public visibility risk: Sports ownership and public incidents can create lasting reputational issues.

- Family office opacity: Less public scrutiny can hide certain governance or liquidity constraints from outside observers.

Comparison: Mark Stevens vs. a typical late-stage VC partner

| Feature | Mark Stevens | Typical Late-Stage VC Partner |

| Background | Engineering + Harvard MBA; semiconductor focus. | Varied (finance, ops, product). |

| Investment style | Concentrated, board engagement, long horizon. | Often diversified across many companies/funds. |

| Vehicle | S-Cubed Capital (family office) + selective board roles. | Institutional funds with LP commitments. |

| Public profile | Low-profile except for major events; notable NBA incident (2019). | Varies widely. |

Examples & brief case studies

Case study: Nvidia

Problem: GPUs were perceived primarily as gaming hardware.

Insight: GPU architecture performs the same dense math needed in modern machine learning.

Action: Early board support, patient holding, influence on strategy.

Outcome: Nvidia became a central AI hardware company; early insiders captured outsized gains.

Case study: Family office move

Problem: Institutional VC Funds require diversification and have fund-life incentives.

Insight: Family capital can be patient and concentrated.

Action: Form a single-family office (S-Cubed) and manage holdings directly.

Outcome: Greater optionality on when to sell and more governance influence in holdings.

FAQs

A: Mark A. Stevens is a venture capitalist, former partner at Sequoia Capital, and the founder of S-Cubed Capital. He has served on the board of Nvidia.

A: Estimates vary. Major outlets list him in the multi-billion-dollar range, mostly because of his early Nvidia stake. These numbers change with the market; treat them as snapshots.

A: Yes. He was an early investor and served on Nvidia’s board during key periods.

A: Stevens joined Sequoia Capital in 1989 and became a partner in the early 1990s.

A: S-Cubed Capital is Stevens’s family office and investment vehicle that manages concentrated public and private holdings.

Final assessment legacy, influence & what to watch next

Mark Stevens’s path illustrates a central idea: deep expertise plus oversight equals exceptional results. His early strong belief in Nvidia, paired with board guidance and the family-office method, reveals how concentrated knowledge and endurance can greatly improve returns for an investor. Meanwhile, public activities (team ownership) heighten public image risks; the 2019 event serves as a warning that prominence carries drawbacks. Looking ahead, monitor S-Cubed’s official reports, Nvidia board updates, and Stevens’s giving efforts at USC for hints of changes in approach, cash access, or fresh investments.

Conclusion

Mark Stevens’s story is a clear, compact lesson in how deep technical knowledge, patient capital, and active governance can combine to create outsized outcomes. He began as an engineer who learned to translate silicon-level tradeoffs into product and market signals, then used that fluency to make concentrated, conviction-driven investments. His early and sustained involvement with Nvidia, not just as an owner but as a director, turned domain insight into real influence and, ultimately, into the headline-generating wealth tied to NVDA’s rise.

That same Playbook also shows the tradeoffs. Running a family office like S-Cubed enabled longer horizons, larger stakes, and more direct governance, but it amplified concentration risk and reduced the transparency that institutional LPs expect. Public-life choices, such as sports ownership, brought prestige and networking benefits and a high-profile reputational cost when personal conduct became news. In short, the levers that create outsized financial returns (concentration, influence, visibility) also increase non-financial vulnerability.

For founders and investors, the practical takeaway is straightforward. If you want to attract Stevens-style capital, speak the technical language clearly, invite governance early, and demonstrate honest risk-management. For investors considering a Stevens-like path, the advice is equally plain: specialize where you can judge truth from noise, take board roles when you can add value, and accept that patience and conviction will sometimes look like stubbornness until they don’t.

Viewed from a long lens, Stevens’s career is less about a single company or incident and more about a repeatable formula: technical depth + governance + time. That formula doesn’t guarantee success, but it explains why certain investors, when they pair expertise with the willingness to stay, can change industries, steer companies, and capture the compounded rewards of patience.