Jonathan Gray: Blackstone’s $1T Architect

Jonathan “Jon” Gray is the executive who transformed Blackstone’s real-estate arm into one of the largest property investment platforms on Earth. Joining the firm as a 22-year-old analyst in 1992, Gray combined dealcraft with systems thinking: sourcing off-market portfolios, centralizing operations, and turning one-off transactions into repeatable, fee-bearing businesses. His fingerprints are on headline transactions, most notably the Hilton leveraged buyout, and on platform creations such as Invitation Homes, the institutional single-family rental company built from post-2008 distressed housing. Over time, Gray expanded his remit from real estate into firmwide strategy as President & COO, emphasizing recurring fee income, private credit, and thematic sectors like logistics and data centers.

This longform profile traces his upbringing, rise inside Blackstone, signature deals, operational playbook, controversies, philanthropic work, net-worth picture, and what Gray’s leadership implies for investors, communities, and regulators. The piece is structured for fast scanning (quick facts, timeline, head-to-head comparisons) and deep reading (playbook, sector pivots, lessons).

Quick facts

- Full name: Jonathan D. Gray (commonly Jon Gray).

- Born: 1970 (commonly reported; specific day varies between sources).

- Role (2026): President & Chief Operating Officer, Blackstone.

- Education: University of Pennsylvania, Wharton School (BS in Economics) and College of Arts & Sciences (BA in English).

- Known for: Architecting Blackstone’s global real-estate platform; leading the Hilton leveraged buyout; creating and scaling Invitation Homes; championing fee-bearing strategies across the firm.

Childhood & early life

Jonathan Gray grew up in suburban Chicago in a household that emphasized academic achievement and professional discipline. He matriculated to the University of Pennsylvania, splitting his studies between quantitative finance/business at Wharton and the humanities in Penn’s College of Arts & Sciences, an early sign of the blend between analytical rigor and narrative framing that would mark his career. In 1992, at roughly 22 years old, Gray joined Blackstone as an analyst. The early 1990s were a formative era for private equity and institutional real estate; Gray learned valuation, structuring, and the nuts-and-bolts of closing complicated transactions. Those first years gave him both a toolset for deal execution and an appetite for building systems that could scale.

Career journey: the step-by-step rise inside Blackstone

Early years: analyst to dealmaker (1992–2004)

Gray’s formative professional path followed a classic investment-banking / private-equity apprenticeship. He absorbed technical valuation and negotiation skills and learned how to manage counterparties, lenders, and operating partners. Importantly, Gray developed an orientation toward value creation that was not purely financial operational improvement; tenant engagement and centralized property management began to appear as levers alongside capital structure.

Building the real-estate engine (2005–2011)

By the mid-2000s, Gray was a senior leader within Blackstone’s real-estate business. Three structural moves defined this phase:

- Centralized asset management. Blackstone aggregated property oversight into professional management teams rather than leaving performance to disparate local owners. Centralization improved leasing outcomes, capital deployment, and cost control.

- Fundraising systems. Gray helped design channels to raise large institutional pools from pensions, sovereign wealth, and large endowments. Those relationships underpinned the scale required to pursue megadeals.

- Diversification of property types. The group expanded beyond core office and retail into logistics, industrial, student housing, and later data centers positioning Blackstone to capture secular tailwinds such as e-commerce.

These moves converted dealmaking skill into a repeatable platform the difference between a firm that does big one-off transactions and a firm that can reliably originate, operate, and monetize entire verticals.

From real-estate chief to firmwide leader (2011–2018+)

Gray’s remit broadened beyond property. He pushed Blackstone to emphasize fee-bearing sources of revenue, private credit, infrastructure, and scalable asset management alongside traditional carried interest. In 2018, he was promoted to President & COO, a role that made him a principal steward of firm strategy and signaled his standing as an internal candidate to ultimately succeed the CEO. The promotion formalized Gray’s transition from platform builder in real estate to enterprise strategist across asset classes.

Signature transactions: Hilton and Invitation Homes

The Hilton leveraged buyout (2007): why it matters

The 2007 acquisition of Hilton is a commonly cited landmark in modern private equity because it combined scale, timing, and operational work. Blackstone purchased Hilton in a leveraged buyout just before the global financial crisis. The ensuing downturn tested ownership: travel demand collapsed, financing markets froze, and balance sheets were strained across the industry. Blackstone’s approach of operational focus, portfolio optimization, and eventual public markets exit via IPO and selective asset sales turned the initial purchase into a substantial success. The Hilton story is used as a case study in patient capital, active ownership, and timing exits to maximize public market appetites.

Why the deal matters (short list):

- Demonstrated Blackstone’s ability to manage complex, global hospitality assets.

- Validated operational investment as a complement to capital structure.

- Delivered outsized returns that funded later firm growth and institutional credibility.

Invitation Homes scaling single-family rentals (post-2008)

After the 2008 housing crash, Blackstone acquired tens of thousands of foreclosed single-family homes, renovated them, and aggregated them into a professional rental business: Invitation Homes. The thesis was straightforward: home values had been impaired, but the rental market was durable; buy, rehabilitate, operate at scale, and create a managed, institutional rental asset.

Why it matters:

- Created, arguably for the first time at scale, an institutional asset class out of single-family homes.

- Showed that Wall Street capital could professionalize fragmented housing stock.

- Sparked political and social debate about the role of private capital in housing and the potential effects on Homeownership.

Quick contrast: Hilton = a single, transformative hospitality platform turned public; Invitation Homes = the creation of a new institutional rental category built from many small, distributed assets.

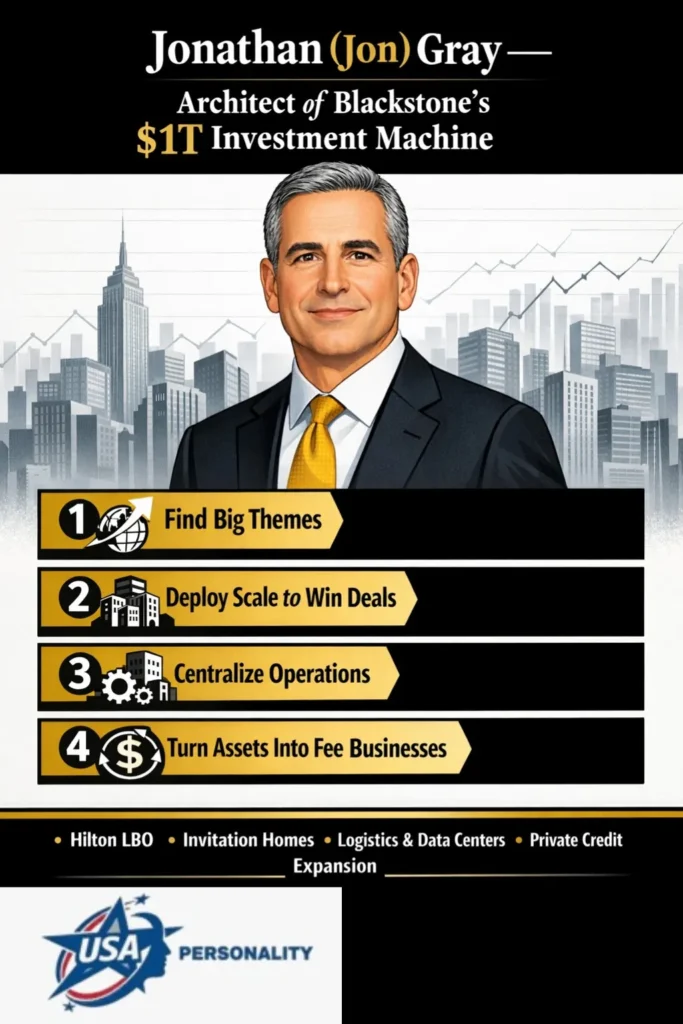

How Jon Gray built Blackstone’s real-estate engine: the playbook

Think of Gray’s method as a structured recipe that converts ideas into a machine.

Step: Find big themes (identify secular tailwinds)

Gray hunts long-running demand trends (e-commerce → logistics, cloud growth → data centers, demographic shifts → housing demand). Betting on structural demand reduces reliance on cyclical timing and improves earnings visibility.

Step: Use scale to win deals

Blackstone’s capital base allows it to outcompete smaller bidders, underwrite entire portfolios, and close quickly. Scale also means offering sellers certainty of close a valuable negotiating lever.

Step: Centralize operations and improve asset performance

After acquisition, Blackstone deploys centralized property management, procurement, leasing playbooks, and capital-improvement programs. The operating uplift often accounts for a large share of value creation.

Step: Turn assets into fee businesses

When a strategy proves repeatable, the firm forms funds or public vehicles that collect management fees and, sometimes, performance fees. This converts volatile one-time profits into predictable recurring revenue.

Step: Exit when markets are ready

When public markets reward the growth/Scale Profile, Blackstone exits via IPO, strategic sale, or refinancing. The Hilton IPO is a classic example.

Step: Repeat and diversify

Successful platforms are scaled into new geographies and adjacent sectors, which diversifies risk and compounds fee revenue.

This playbook is mechanical and iterative: theme → buy at scale → operate → institutionalize → exit → repeat.

Sector pivots: logistics, data centers, and private credit

Gray’s sense of durable demand led Blackstone to push into sectors where structural growth and high barriers to entry create durable cash flows.

- Logistics & industrial: E-commerce changed real estate demand. Last-mile distribution, large fulfillment centers, and cold storage became preferred property types. Blackstone’s capital allowed it to assemble and modernize logistics portfolios quickly.

- Data centers: The rise of cloud computing, streaming, and AI drove persistent demand for highly specialized infrastructure. Data centers can offer contractual cash flows and attractive long-term leasing economics.

- Private credit: By building private lending platforms, Blackstone created fee-bearing, asset-backed income streams that sit alongside public and bank financing and that benefit from the firm’s origination and underwriting scale.

Each pivot follows the same Gray logic: identify secular demand, commit scale, professionalize operations, and convert returns into fee income where possible.

Net worth, income sources, and financial picture

Public trackers list Jon Gray among billionaires, but precise figures vary with market moves and reporting methodology. His wealth is a composite of:

- Equity holdings in Blackstone stock fluctuate with the market.

- Carried interest from funds he helped originate and manage (often realized over fund life cycles).

- Direct compensation (salary, bonuses, incentive pay).

- Board and advisory fees and other outside income.

For up-to-date net-worth figures, consult Bloomberg, Forbes, or other live wealth trackers; public estimates are snapshots that change when valuations or personal liquidity events occur.

Controversies & public scrutiny: a short, honest view

Gray’s scale invites scrutiny both because of the size of capital under management and because real estate and credit interact with communities in tangible ways.

Housing backlash

Critics argue that the institutional purchase of single-family homes after 2008 made it harder for individual buyers to purchase entry-level housing and, in some areas, put upward pressure on rents. Defenders counter that institutional landlords brought professional management, capital for repairs, and a stable rental supply to markets where housing stock was distressed.

Private credit and regulatory questions

As non-bank lending grows, questions arise about oversight, borrower protections, and systemic risk. Blackstone and its peers argue private credit fills a gap left by constrained bank balance sheets and offers carefully underwritten alternatives; regulators and watchers remain interested in whether rapid growth requires different oversight.

Reputational balance

Gray and Blackstone emphasize fiduciary duty to investors and legal compliance. Still, when institutional capital intersects with essential services like housing, political and reputational considerations become part of the strategic calculus.

Personal life & philanthropy

Gray maintains a relatively private personal life. He and his wife, Mindy, are philanthropic, supporting medical research and educational causes through family foundations and gifts. Their giving underscores a pattern common among major finance figures: deploying private wealth toward public goods, often with a focus on health and learning.

Timeline

| Year | Milestone |

| 1970 | Born (commonly reported year). |

| 1992 | Joins Blackstone after UPenn. |

| 2005 | Rising to lead/co-head roles in global real estate (approx.). |

| 2007 | Led Blackstone’s leveraged buyout of Hilton. |

| 2008–2012 | Led post-crisis portfolio acquisitions and Invitation Homes build-out. |

| 2018 | Promoted to President & COO of Blackstone. |

| 2023–2026 | Continues to push Blackstone into AI-infrastructure, private credit and logistics. |

Head-to-head: Jon Gray vs. a traditional private-equity CEO

| Feature | Jon Gray (Blackstone) | Traditional PE CEO |

| Background | Real-estate + institutional fundraising; platform builder. | Buyouts, industry roll-ups, corporate carve-outs. |

| Business model | Multi-asset manager; emphasis on recurring fees and scale. | Often focused on deal-level carry and operational turnarounds. |

| Public issues | Housing politics, private credit oversight, systemic implications from scale. | Varies sometimes scrutiny around layoffs, restructurings, and bankruptcy outcomes. |

| Strength | Scale, diversified fee base, platform repeatability. | High single-deal upside; concentrated value extraction on specific targets. |

Lessons: what founders and investors can learn

- Systems beat heroics. Deals are important, but the scalable processes that let you repeat a thesis are what create lasting firms.

- Operational rigor is a force multiplier. Improving operations (management, procurement, capital projects) can produce returns beyond financial engineering.

- Think thematically and act with conviction. Gray’s success stems from committing to durable themes and building the infrastructure to serve them.

- Convert wins into predictable economics. Turning a successful strategy into fee-based vehicles reduces volatility and increases enterprise value.

- Scale carries responsibility. When capital gets large enough to affect markets (housing, credit), stakeholder management and public policy engagement become essential.

FAQs

A: As of 2026, Jonathan Gray is President & Chief Operating Officer and is often mentioned as a likely internal candidate to succeed CEO Stephen A. Schwarzman.

A: The Hilton leveraged buyout (2007) is widely seen as his signature transaction and one of the most successful hotel deals in private equity history.

A: Invitation Homes scaled institutional ownership of single-family rental homes after 2008. Critics argued it reduced homeownership access in some markets; supporters said it professionalized and repaired large numbers of damaged homes.

A: Estimates vary. Public wealth trackers like Bloomberg and Forbes list him in the billionaire range, but figures change with markets and distributions. For live numbers, consult Bloomberg or Forbes.

Conclusion

Jonathan “Jon” Gray is a modern platform builder: he took dealmaking skill and amplified it through systems, operations, and institutional fundraising. By converting transactions into repeatable businesses, Gray changed Blackstone’s economics, increasing fee income and diversifying sources of profit beyond single-deal carry. The approach made Blackstone more resilient and positioned it to capitalize on structural trends like e-commerce, cloud computing, and non-bank lending. But scale brings scrutiny: when institutional capital touches housing, credit, or essential infrastructure, regulators, communities, and politicians take notice. For Investors and operators, Gray’s career is both a blueprint for building an asset-management machine and a cautionary note about the social responsibilities that come with market-moving capital.