Dan Friedkin: Business & Conservation

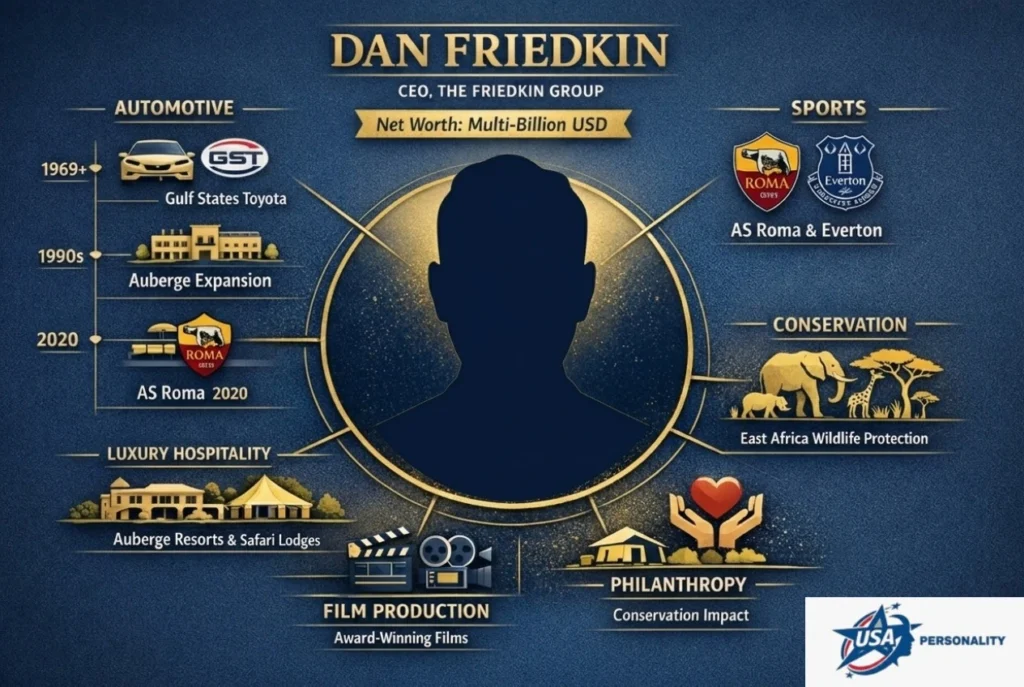

Dan Friedkin is a low-profile but highly influential American entrepreneur whose family wealth sits inside a private holding structure rather than a public company. His profile now spans automotive distribution, film and entertainment, luxury hospitality, sports ownership, and conservation — and the 2024 Everton takeover, plus the club’s 2026 stadium financing, made that broader strategy much more visible to readers and search engines alike.

For readers, the key question is simple: how did Dan Friedkin build this kind of reach? The short answer is that the family’s long-running cash engine is Gulf States Toyota, one of the world’s largest independent distributors of Toyota vehicles and parts, while The Friedkin Group acts as the private platform that deploys that cash into long-duration assets such as Auberge Collection, AS Roma, Everton, and East Africa conservation work.

Quick summary

This pillar guide is a long-form, plain-English explainer designed to satisfy multiple search intents: biography, net worth, corporate profile, sports takeover, and conservation reporting. It’s written in a structured, NLP-friendly fashion so sections map to user intents (Who → Entity, How → Mechanism, When → Timeline, Why → Strategy, FAQ → Slot answers). That makes it useful to casual readers, analysts, and publishers who want a publish-ready structure (schema-ready, with obvious places for Article, Organization and FAQ JSON-LD).

Quick facts

- Full name: Thomas Dan Friedkin

- Born: February 27, 1965

- Main roles: Chairman & CEO, The Friedkin Group; Owner/Chairman (majority) of Everton Football Club (acquisition completed December 2024)

- Base: Houston, Texas

- Core business: Gulf States Toyota (GST) regional Toyota distributor

- Known for: Automotive distribution, film production credits, conservation projects in East Africa, luxury hospitality, sports ownership

- Net worth: Multi-billion USD (estimates vary; range-based due to private holdings)

(When publishing: include a “Last updated” date beside net worth and cite the primary sources used to estimate.)

Childhood and early life

Dan Friedkin grew up inside an entrepreneurial family with aviation and regional business interests. He studied at Georgetown University and Rice University and then returned into the family business environment. Early exposure to aviation and travel influenced later investments in aircraft, hospitality and experiential travel lodges. From an entity-relationship perspective: family → GST (core business) → Friedkin Group (holding) → diversification (hotels, sports, conservation).

How Dan Friedkin made his money

The principal source of the Friedkin family’s wealth is Gulf States Toyota (GST). GST is a regional automotive distributor: it purchases inventory from Toyota and supplies a network of retail dealers across several U.S. states. The economics of a large authorized distributor are simple in structure:

- Volume: High unit sales create scale.

- Margins: Stable per-vehicle margins and manufacturer incentives.

- Network effects: Long-term relationships with dealers and localized market intelligence.

- Predictability: Consistent cash generation that funds other, less-liquid investments.

Think of GST as the cash engine (core node). The Friedkin Group uses that predictable cash flow to Invest in capital-intensive, headline assets sports clubs (Everton), luxury hospitality brands (Auberge Resorts, safari lodges), and long-term conservation projects. From a risk-model viewpoint, a stable distributor reduces the probability of cash shocks and creates optionality for strategic purchases.

What is the Friedkin Group?

The Friedkin Group is the private family holding company that aggregates the Family’s Assets. For content modeling, treat it as an Organization entity with multiple business units (automotive, hospitality, aviation & media, sports, conservation).

Major parts of the group

- Automotive distribution: Gulf States Toyota (GST) core cash generator.

- Hospitality: Auberge Resorts collection and private luxury safari lodges.

- Aviation & media: Private aircraft holdings, aviation operations, and film production credits.

- Sports: Ownership stakes including AS Roma (family stake) and Everton (majority stake completed Dec 2024).

- Conservation: Land protection, eco-lodges and community partnership projects notably in Tanzania.

The operating idea

- Maintain a stable cash-generating core GST.

- Deploy capital into differentiated, long-duration assets (hotels, sports clubs, conservation).

- Build cross-sector synergies (VIP hospitality for sports guests, storytelling via film/media, conservation-linked eco-tourism).

- Use high-touch luxury experiences to create premium margin niches that sustain protected lands.

From an NLP standpoint, this is a classic hub-and-spoke model where the core hub (GST) underwrites spokes that have both revenue and reputational value.

Everton takeover: what happened and why it matters

In December 2024, the Friedkin family completed the purchase of a controlling stake in Everton Football Club. The transaction shifted ownership control to the Friedkin Group and signalled a move into high-profile European sport.

Simple timeline of the Everton deal

- 2023–2024: Negotiations and due diligence.

- December 2024: Takeover completed; Friedkin family acquired a majority stake (reported near ~98.8% in media reporting).

- Immediate priorities post-acquisition: Stabilize the club’s finances and support the Bramley-Moore Dock stadium project.

Why this matters

- Stadium financing: Everton had a stadium development at Bramley-Moore Dock that required significant capital and investor certainty. The takeover improved refinancing prospects.

- Brand & reach: Premier League ownership delivers global brand exposure, commercial revenue channels, and premium hospitality integration.

- Community & risk: Football clubs are community institutions. Effective ownership must balance commercial goals with fan expectations and local identity.

Sports strategy: what the Friedkins want from football

The Friedkin approach appears to be long-term and integrative rather than short-term profit extraction.

Key elements

- Stabilize finances to ensure operations and stadium projects proceed.

- Commercial growth: expand sponsorship, matchday revenues, licensing.

- Hospitality synergies: create premium experiences linking hotels, VIP match packages, and travel guests.

- Community investment: youth academies and local programs to secure social licence.

Risks to watch: cultural mismatch with fans, high operating costs for competitive squads, and reputational risk if community engagement is insufficient.

Hospitality & conservation: how they fit together

The Friedkin Group’s hospitality assets (Auberge Resorts and safari lodges) and conservation projects form a purposeful cluster. The operating hypothesis is:

- Conserve land to maintain biodiversity and unique guest experiences.

- Develop luxury lodges that sell exclusivity and conservation narratives.

- Monetize sustainable tourism so revenue funds park management and Local Development.

- Reinvest conservation proceeds into both social programs and operating capital.

This creates a positive feedback loop: pristine environment → premium guest willingness-to-pay → funds for conservation → preserved environment.

The Friedkin Conservation Fund

The family backs wildlife protection efforts in East Africa, safeguarding vast land areas and developing eco-friendly lodges. These efforts frequently collaborate with nearby residents and authorities to generate shared income sources and job opportunities. The business approach combines earnings from non-destructive activities (tourism) with conservation results (patrol teams, animal safeguarding), improving both environmental and community measures.

Net worth: why numbers vary

Estimating Dan Friedkin’s net worth is challenging because most assets are privately held. Methodologies commonly used by outlets include:

- Top-down proxy: Use GST annual sales and estimated profit margins to infer enterprise value.

- Asset-by-asset: Use disclosed purchase prices for club stakes (e.g., Everton) and estimated valuations for hotels/real estate.

Comparable multiples: Apply EV/EBITDA or revenue multiples from public hospitality and distributor comparables. - Adjust for debt & ownership: Subtract known liabilities and scale by family ownership percentages.

Because these inputs (margins, multiples, debt) are variable, the result is a range rather than a single figure. Good publisher practice: show the range and explain the assumptions, with a transparent “last updated” date.

How Dan Friedkin Turns Private Wealth into Global Influence

Dan Friedkin’s approach goes beyond accumulating assets; it’s about creating influence that spans industries and continents. By using Gulf States Toyota as a stable financial foundation, he strategically invests in Everton, luxury hospitality through Auberge, and conservation in Tanzania. This method demonstrates how a privately held enterprise can drive global impact—blending business acumen with social and environmental responsibility—while offering a model for long-term value creation that resonates with both fans and investors.

Timeline major milestones

- 1960s–1970s: Family roots in aviation and early enterprises.

- 1969 onward: Gulf States Toyota’s growth as a Central Business.

- 1990s–2010s: Expansion into hospitality (Auberge), film, aviation, and conservation.

- ~2020: Family stake in AS Roma (completed earlier).

- Sep–Dec 2024: Negotiations and completion of Everton takeover.

- 2026: Active stadium financing work, conservation expansion, and hospitality integration.

A clear comparison table: Dan Friedkin vs a typical U.S. sports owner

| Feature | Dan Friedkin | Typical U.S. Owner (example) |

| Main cash engine | Gulf States Toyota (stable automotive distributor) | Varies; real estate sometimes presents |

| Sports portfolio | AS Roma (family stake) + Everton (majority) | Often single club, media-linked ownership, or franchise-based |

| Hospitality & conservation | High focus — Auberge, Tanzania lodges | Varies; public companies are more transparent |

| Transparency | Low family office, private | Varies; public companies more transparent |

| Stadium funding | Active with refinancing & capital support | Depends mixes of public & private funding |

Pros & Cons

Pros

- Stable cash flow from GST funds for strategic investments.

- A diversified portfolio across hospitality, sports, and conservation reduces single-sector exposure.

- Conservation + hospitality generates positive PR and sustainable revenue.

Cons

- Private structure creates opacity for external stakeholders.

- Sports ownership involves high emotional and reputational risk with fan communities.

- Operational expertise for football clubs differs from car distribution or hotel operations.

What investors and founders can learn

- Build a reliable cash engine first. Predictable profit streams create flexibility.

- Diversify into complementary verticals. Hotels and sports can create cross-selling Opportunities.

- Invest in reputation. Conservation projects and community programs protect brand equity.

- Communicate proactively. For community-facing assets (sports clubs), early engagement is essential.

How the Friedkin Group generates value

| Business unit | How does it make money | Strategic value |

| Gulf States Toyota (GST) | Distribution margins, volume rebates | Core cash to fund acquisitions |

| Auberge Resorts & Lodges | Rooms, events, F&B, experiences | High-margin hospitality + brand |

| Sports clubs (AS Roma, Everton) | Matchday, broadcast, commercial, transfers | Upside via media & stadium revenue |

| Conservation & lodges (Tanzania) | Eco-tourism stays & partnerships | Sustainable revenue + social license |

| Film & media | Production credits & distribution | Storytelling and PR value |

FAQs

A: Estimates change because many assets are private. Public reports use GST sales and disclosed deals. Most sources list him in the multi-billion-dollar range. Check trusted finance outlets for the latest figures.

A: The Friedkin Group completed its purchase of Everton in December 2024, taking a controlling majority stake and working to stabilise the club and support its stadium plans.

A: Primarily through Gulf States Toyota (GST), the regional Toyota distributor that generates large, steady revenue.

A: The Friedkin family runs conservation projects in East Africa, including protected land and e5co-lodges that help local communities and preserve wildlife.

A: The Friedkin family completed their acquisition of AS Roma earlier and has maintained a stake as part of their sports holdings.

Conclusion

Dan Friedkin’s story is not just about wealth; it is about structure. A steady private business in automotive distribution gives The Friedkin Group the freedom to own and develop assets that are more emotional, more visible, and more long-term in nature — from Everton and AS Roma to Auberge and conservation work in Tanzania. The result is a portfolio built for control, patience, and brand value rather than quick wins.

For readers, that makes the story useful beyond biography. It shows how a family office can turn one durable cash engine into a multi-sector platform with Global Reach. For anyone studying ownership strategy, that is the big takeaway worth following as the portfolio continues to evolve in 2026.