Ernest C. Garcia III: Carvana CEO

Ernest C. “Ernie” Garcia III is the co-founder and chief of Carvana, the online pre-owned car platform recognized for always-on listings, broad photo tours, and viral vehicle “vending displays.” Under his direction, Carvana expanded rapidly, went public in 2017, and later became the focal point of heavy scrutiny over funding setups, related-party agreements, and lawsuits. This guide outlines his history, reframes Carvana’s operation as a processing pipeline, provides a chronological timeline, summarizes the main Hindenburg allegations and Carvana’s responses, covers legal probes, and delivers a plain-language forecast for 2026 with practical signals for reporters and investors. Primary sources include SEC filings, the Hindenburg dossier, BloombergLaw reporting, Carvana shareholder updates, and live wealth tracking tools.

Quick facts

- Full name: Ernest C. Garcia III (commonly Ernie Garcia).

- Role: Co-founder and Chief Executive Officer of Carvana.

- Born: Public sources list 1982–1983 (≈ 42–43 in 2026).

- Education: Stanford University, B.S., Management Science & Engineering (2005).

- Base/residence: Phoenix / Tempe, Arizona area (Carvana HQ and family base).

Childhood, education, and early career latent features and formative priors

Ernest Garcia III grew up within a family structure already deeply tuned for pre-owned car retail. His father, Ernest Garcia II, developed DriveTime (first called Ugly Duckling) into a nationwide used-car chain. That family background acted as an initial guide: early contact with inventory cycles, auto loans, repossessions, and regional markets embedded practical knowledge into Garcia III’s decision-making process.

After finishing at Stanford in 2005 with a degree in Management Science & Engineering, a course blending numerical modeling and systems analysis, Garcia III worked in finance and principal investing, positions that refined his skills in capital deployment and structured deals. In 2007, he transitioned to DriveTime operations; that hands-on training provided the working playbook he later adapted into an online, vertically integrated platform.

Consider this early stage as model initialization: experience, networks, and capital access supplied priors that shaped how the Carvana structure would be designed and optimized.

How Carvana works: pipeline view

Reframe Carvana as a production data pipeline whose “data points” are vehicles and whose output is completed retail transactions plus ancillary finance revenue. The platform comprises discrete stages, each transforming the asset and adding information (features) and value.

Ingestion (Source cars): Vehicles enter the system from auctions, trade-ins, wholesale buybacks, and direct acquisitions. This is the raw dataset, a noisy stream with varying provenance and quality.

Preprocessing (Reconditioning): At centralized reconditioning centers, vehicles undergo mechanical remediation, cosmetic repair, cleaning, and standardized photographic capture (high-res images and 360° tours). This is data cleaning, normalization,n and augmentation, making disparate inputs comparable and more saleable.

Feature extraction (Listing & metadata): Each car is annotated with structured attributes (mileage, trim, VIN history, condition scores) and unstructured assets (image tours). Pricing models and heuristics assign list prices. This stage exposes the condition, history,and desirability that the marketplace uses to rank, price, and recommend.

Inference & serving (Sell and deliver): Customers interact via the web UI, select financing options, and elect delivery or pickup (including the branded vending-machine experience). The Platform’s “inference” is the match between consumer demand and vehicle supply, underwritten by pricing and credit models.

Monetization layer (Finance & F&I): Carvana offers in-house financing, warranties, and add-on products (GAP, protection packages). These post-sale products increase lifetime value and yield complexity analogous to downstream revenue modeling and retention strategies.

Why view it this way? This pipeline framing clarifies where value is created and where model risk concentrates. Vertical integration, owning sourcing, reconditioning, listing, and financing, yields tighter feature control and potential margin capture. But the same verticalization centralizes capital and liquidity exposure: inventory carrying requires financing; in-house loans require credit risk models and securitization. If exogenous covariates (used-car prices, macro credit conditions) shift, the pipeline’s assumptions can break, leading to pthe ropagation of errors and amplified losses.

The growth story (2012 → 2021) training, amplification, and reach

2012 Launch: Carvana began as a DriveTime spin-out. Founding team: Ernest Garcia III, Ryan Keeton, Ben Huston. Initial architecture prioritized user experience and standardized vehicle presentation.

2017 IPO: Listing on public markets was a regime change. Public capital enabled rapid scale, more inventory, more logistics nodes, bigger marketing, and more vending-machine installations. The IPO also introduced external supervision (shareholder expectations, public disclosure cadence), forcing the company to model growth projections for outside stakeholders.

2019–2021 Pandemic training environment: The pandemic generated a unique training dataset: supply chain constraints, rental fleet retirements, and shifting consumer behavior propelled used-car prices higher. Carvana’s online UX and 360° tours, supported by pandemic-era demand for contactless buying, amplified adoption. Revenue and unit growth spiked. Simultaneously, the Garcia family executed notable insider stock sales (documented across filings and press coverage), large dispositions that later became a focal point for governance questions.

Takeaway: The Carvana model achieved product-market fit in a particular macro environment. The system accrued technical and network advantages (brand awareness, logistics), but also accumulated leverage and dependence on favorable macro covariates, an implicit model assumption that would be stress-tested when the environment normalized.

The fall and the recovery (2022 → 2024) dataset shift and remediation strategies

After the strong 2019–2021 period, outside factors shifted:

1: Price correction: Transaction and wholesale used-car values reverted toward averages as pandemic effects faded.

Credit squeeze: Lenders tightened loan rules, raising borrowing costs and limiting consumer access.

2: Funding limits: Carvana held large inventory and depended on capital markets and securitizations to fund loans and purchases. Those funding sources shrank when risk premiums increased.

3: These changes caused a structural shift in the operating environment. The market reassessed the company, and the CVNA stock dropped in 2022, sharply lowering headline net worth estimates for Garcia and associated parties.

Recovery and stabilization (2023–2024): Carvana acted with several model updates and operational adjustments: staff cuts, asset allocation tweaks (fewer expansion projects; faster inventory turns), debt reorganizations, and stricter unit economics. Management aimed to improve gross margins per vehicle and protect cash flow. These measures helped stabilize key metrics, though legal, reporting, and governance concerns lingered as ongoing background issues continued to affect risk premiums and capital access.

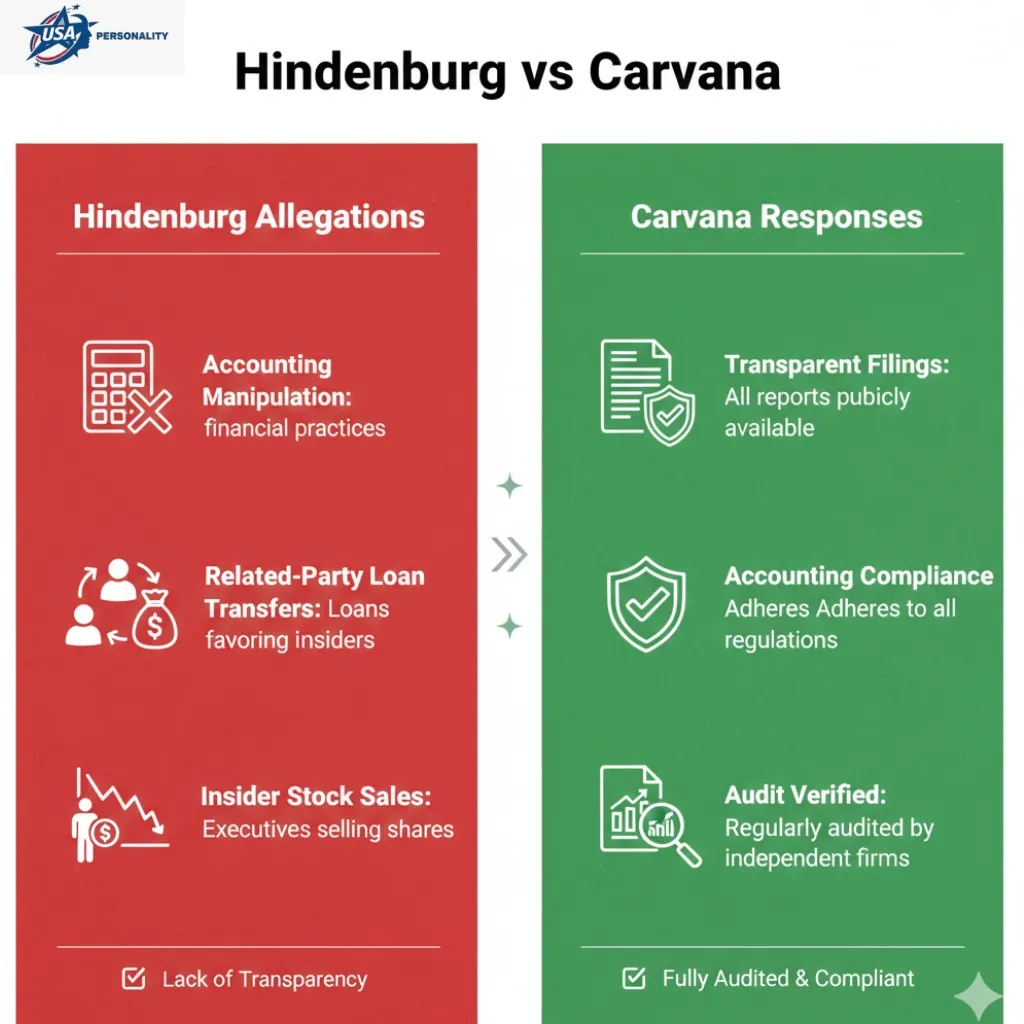

The Hindenburg report (Jan 2, 2025) adversarial example and key claims

On January 2, 2026, short-seller Hindenburg Research published a detailed probe titled “Carvana: A Father-Son Accounting Scam For History.” Treat this paper as a critical input: a deliberately negative, high-impact piece aimed to shake market confidence.

Hindenburg’s main claims

1: Accounting distortion: Hindenburg argued that Carvana exaggerated some metrics and hid loan performance, similar to misreporting signals that could skew model outcomes.

2: Family-linked loan shifts: The report alleged undisclosed or unclear loan moves to entities tied to the Garcia family—transactions Hindenburg said were significant and poorly revealed. The document valued these moves in hundreds of millions.

3: Insider equity timing: Hindenburg noted major Garcia family stock sales while public statements painted positive results, creating perception of unequal access and possible conflicting incentives.

Carvana’s reply

The company publicly called the document “false and misleading,” defended its accounting and disclosures, and stressed that filings and audits met all rules. Carvana urged readers to rely on primary records (SEC filings) for a verified account. Independent journalists later analyzed both Hindenburg claims and Carvana rebuttals.

How to read adversarial papers

Short-seller reports are negative by design—the authors profit if the stock drops. That incentive creates bias risk. Still, these reports can reveal real, previously missed signals or audit trails. The smart method: treat the report as a starting point and cross-check with official filings (10-Ks, 10-Qs), auditor notes, court records, and neutral third-party sources before final conclusions.

Legal probes, shareholder suits, and Delaware court actions are the investigation pipeline

Following the Hindenburg publication (and earlier concerns), multiple legal threads advanced:

- Shareholder litigation: Plaintiffs consolidated claims alleging inadequate disclosure on insider sales and related-party transactions. These suits seek damages or corporate governance remedies and can trigger discovery that uncovers internal communications and transactional details.

- Delaware Chancery & derivative actions: Courts and special litigation committees reviewed whether directors or controlling shareholders breached fiduciary duties. BloombergLaw and other legal outlets tracked motions, privilege disputes, and dismissal orders through 2024–2026. Some motions to dismiss were filed and adjudicated; in some cases, courts affirmed dismissals. But dismissal at an early stage does not necessarily preclude further discovery or other claims.

- Regulatory inquiries: Where applicable, regulatory agencies may scrutinize disclosures, accounting practices, or securitization structures; these are slower-moving but can impose civil or administrative consequences.

Why litigation matters as a signal: Litigation is part truth-finding, part discovery exercises. Even if a case is dismissed, the process imposes legal fees, management distraction, and reputational friction, and disclosure during discovery can surface new facts. For risk modeling, pending litigation increases tail risk and, for public companies, increases the cost of equity and borrowing.

Net worth (2026): Why Garcia’s headline number jumps around

Estimating an individual’s Net Worth when most holdings are equity is inherently volatile. Key reasons for large swings:

- Concentration in public stock: A significant portion of Garcia’s wealth is tied to CVNA shares and family holdings connected to DriveTime. Public equity values change intraday.

- Leverage & pledged stock: If founders pledge shares or use them as collateral, market moves can create forced selling or liquidity stress, further feeding volatility.

- Real-time trackers: Sources like Forbes and Bloomberg compute daily snapshots based on market price and reported holdings so reported net worth is a point estimate susceptible to high variance. Always include the date and the source when citing a net-worth figure.

Practical rule for reporters: When reporting a net-worth number, show the date and the calculation basis (shares × price, less known liabilities) and, if possible, provide a sensitivity table showing how wealth would change with ±10% moves in share price.

Leadership style strengths and weaknesses

Strengths

- Product orientation: Garcia emphasized a user-first digital experience, high-quality imagery, a streamlined buying journey, and logistics innovation (vending machines), all tangible product signals that drove adoption.

- Vertical control: By integrating sourcing, reconditioning, and financing, Carvana captured multiple margin points and controlled feature quality across the pipeline.

Weaknesses

- Capital intensity: Heavy leverage and in-house financing increase sensitivity to interest rates and funding markets; a small shock in funding costs can magnify into a cash-flow problem.

- Governance optics: Family control, insider sales and opaque related transactions created governance friction, increasing informational asymmetry and negative narratives that raised the firm’s risk premium.

Synthesis: Garcia built a differentiated, consumer-facing model with operational ingenuity. But the model’s dependence on external finance and complex securitization pathways plus governance optics left the company vulnerable to narrative shocks and capital-market retrenchments.

Timeline table life & company milestones

| Year | Event |

| c.1982–1983 | Ernest C. Garcia III born (public records list 1982–83). |

| 2005 | I graduated from Stanford University (B.S., Management Science & Engineering). |

| 2007 | Joined DriveTime (operational and finance roles). |

| 2012 | Carvana was founded (co-founder; early product & logistics buildout). |

| 2017 | Carvana IPO provides public capital access and rapid expansion. |

| 2019–2021 | Pandemic surge: pricing spikes, demand surge, and accelerated unit growth; notable Family insider stock sales. |

| 2022 | Market re-pricing and stock collapse; liquidity and margin pressures. |

| 2023–2024 | Restructuring, cost reduction, asset optimization and tightened unit economics. |

| Jan 2, 2026 | Hindenburg Research publishes a major short-seller report alleging accounting and related-party issues. |

| 2026(ongoing) | Delaware probes, shareholder litigation, regulatory interest and continued market trading. |

FAQs

A: Yes, Ernest C. Garcia III is a co-founder and the CEO of Carvana.

A: Hindenburg alleged accounting manipulation, undisclosed related-party loan sales and big insider stock sales by the Garcia family. Carvana denied the report. Read both the Hindenburg report and Carvana’s filings for primary evidence.

A: Net worth changes daily with CVNA stock. Forbes and Bloomberg publish real-time estimates and always record the date when you cite a number.

A: Yes. Shareholder suits and Delaware court actions have examined insider sales and related disclosures; some cases have had rulings but litigation and discovery continued into 2026.

A: Carvana’s Investor Relations page and SEC filings (Form 10-K, 10-Q) are the best primary sources.

Conclusion

Ernest C. “Ernie” Garcia III is a unique mix of product creator and sector insider: he combined deep industry knowledge gained from DriveTime, paired it with a digital-first product mindset, and scaled Carvana into a nationally known brand that changed how Americans purchase used vehicles. That success, building a distinct user experience, a logistics network, and an integrated financing system, is a lasting credential and explains why Carvana drew strong investor attention and rapid expansion.

Garcia’s fast-growth strategy boosted control and margins but increased capital demands, exposure to market shifts, and governance scrutiny. Hindenburg reports, lawsuits, and net-worth swings reflect these trade-offs. Looking ahead, Carvana may stabilize and regain trust, face ongoing legal and market pressures, or follow a hybrid path of modest recovery amid continued governance fixes.

For journalists and investors, the practical lesson is clear: assess Garcia’s record as a mix of tangible product success and built-in model risk. Track hard indicators — SEC filings, audit notes, loan data, and Delaware court filings — instead of relying on headlines or single-source adversarial reports. Ultimately, Ernest Garcia’s Legacy will be measured by whether Carvana can convert operational innovation into lasting economics under transparent governance.